I had a founder tell me once that the scariest moment in his first year was opening his bank app on a Tuesday morning and seeing $600, two days before payroll.

Nothing looked wrong on paper. His income statement had shown $40,000 in profit that quarter. Sales were solid, margins held up. And yet there was no cash.

I've watched this cash flow vs. profit confusion stop first-time founders cold. Most people searching for profit vs. cash flow are really asking the same question: why does my business look healthy on paper but feel broke in practice?

I’ll walk you through exactly how both work, why that gap shows up even when sales are strong, and how to build financial projections that account for both in your business plan.

What is cash flow?

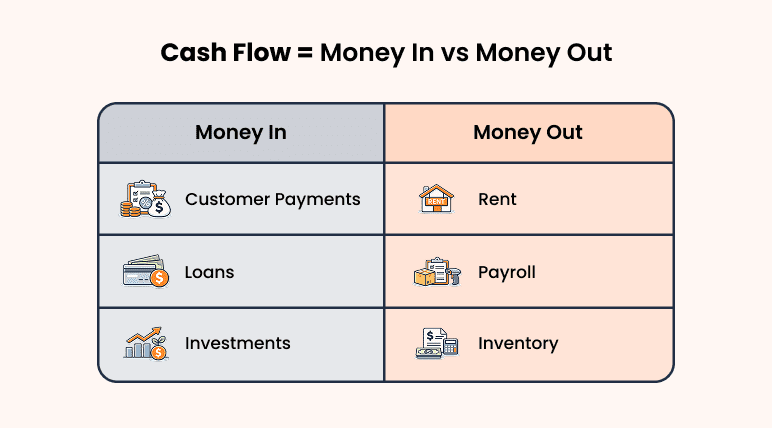

Cash flow is the money moving in and out of your business, based on when cash actually hits or leaves your account.

The simplest way I explain it to founders is this: your bank balance at any given moment is your cash position. It doesn't care what your income statement says. It only reflects what has actually arrived and what has actually left.

Cash comes in from:

- Customer payments when received

- Loan proceeds when deposited

- Investor funding when transferred

Cash goes out through:

- Rent, payroll, and operating expenses when paid

- Equipment purchases paid upfront

- Loan repayments, including principal that doesn't show as an expense

Positive cash flow means more is coming in than going out. Negative means the reverse. That number tells you whether the business can operate this week, regardless of what the P&L says.

Track your cash flow weekly, not monthly. Monthly reports often hide mid-month dips, and that's usually when payments get missed. And when you do review it, don't just look at the total balance. Look at where the cash is actually coming from.

What is profit?

Profit is what your business earns after all costs and expenses are subtracted from revenue over a specific period of time. It tells you whether the business is generating more than it spends.

If you buy $25,000 in inventory, only the portion you've sold shows up as a cost that month. The rest sits on your balance sheet. If you repay a loan, only the interest qualifies as an expense. The principal leaves your account with no trace on the P&L. If you buy equipment, the cost gets spread across years, not recorded all at once.

In each case, the cash moved, but the profit stayed the same.

This is why two businesses with identical profit figures can be in completely different cash positions. Profit tells you what accounting records. It doesn't tell you what was actually left in your bank account.

In my experience, most founders just watch net profit and stop there. But gross margin is usually where the real problem is hiding. If your pricing is off, no amount of cost-cutting fixes it later.

Gross profit margin tells you if your pricing works. Net profit margin tells you if your business works. You need both numbers

Cash flow vs. profit — Side-by-side comparison

Profit tells you if your business model works. Cash flow tells you if you can pay your bills this week.

They're connected, but they answer very different questions. I find the easiest way to see it is side by side.

| Aspect | Cash flow | Profit |

|---|---|---|

| What it measures | Actual movement of money in and out | Revenue minus expenses |

| Reported on | Cash flow statement | Income statement (P&L) |

| Timing | When cash is received/paid | When revenue is earned, and expenses are incurred |

| Includes | Customer payments, loan inflows, asset sales | Revenue and operating expenses |

| Excludes | Non-cash items like depreciation | Loan repayments, asset purchases |

| Can be positive while the other is negative | Yes | Yes |

| Best indicator of | Short-term liquidity | Long-term business viability |

Two things explain most of the gap between these numbers.

Timing

Profit runs on accrual accounting. Revenue is recorded when you earn it, not when the money actually arrives. The same goes for expenses. So you might book $30,000 in revenue this month, but if customers pay net-60, your income statement looks healthy while your bank account is still waiting.

The IRS outlines accrual vs cash accounting methods if you want to understand how this applies to your business specifically.

Non-cash and non-operating items

Not every cash movement shows up as an expense, and not every expense affects cash. Loan repayments are the clearest example. When you repay a $2,000 loan installment, the full $2,000 leaves your account. But only the interest portion, maybe $500, shows up on your income statement. The remaining $1,500 in principal reduces your cash with no trace on your P&L.

Depreciation works the opposite way. It reduces your profit on paper, but no cash actually leaves your account when it's recorded.

This is exactly why I tell founders not to rely on a single number. Your P&L can look fine while your cash is under pressure. Free cash flow, which is operating cash minus capital expenditures, is the cash actually available to pay debt or reinvest. That number often tells a more complete story than either profit or cash flow alone.

Why is cash flow the king?

For any business, profit is the goal at the end of the day. But cash flow is what keeps you in the game long enough to reach it.

You can delay hiring. You can negotiate payment terms. You can cut non-essential costs. What you cannot do is delay payroll, miss a rent payment, or tell a supplier to wait indefinitely. All of those obligations run on cash.

Cash flow is also what determines every growth decision you make:

- Taking on a new client depends on whether you can cover costs before they pay you.

- Hiring depends on whether payroll clears next month, not whether the annual P&L looks healthy.

- Negotiating supplier terms depends on how much cash you have available right now, not what your income statement shows.

- Investing in growth depends on whether cash is available when the opportunity appears, not whether last quarter was profitable.

Lenders understand this better than most. When you apply for a loan, they look at cash flow before they look at profit. It tells them whether the business can actually make repayments, regardless of how profitable it looks on paper.

Why a profitable business can still run out of cash

I've seen businesses post a solid profit and still scramble to make payroll that same week. The gap usually comes down to one of three things.

1) Slow-paying customers

A consulting firm wraps up a project in March. They invoice $30,000. Monthly expenses run $20,000. The books show a $10,000 profit. But the client is on net-60.

So the money won't arrive until May. Meanwhile, rent is due, payroll runs, and the business is covering its own costs while it waits.

| Month | Profit (in $) | Cash flow (in $) |

|---|---|---|

| March | +10,000 | -20,000 |

| April | 0 | -20,000 |

| May | 0 | +10,000 |

Two months of operating in the red, on a deal that was technically profitable from day one. When the payment finally arrived, it barely covered what had already gone out.

2) Inventory before sales

A retail business drops $25,000 on inventory in January for a spring launch. That cash is gone immediately. But it doesn't hit the income statement until the products actually sell, which might be March or April.

- January cash: -$25,000

- January profit: $0

The expense only hits the income statement when the products sell in March. So for two months, the business has less cash, but the books don't show a loss yet.

3) Loan repayments

A business is paying a $100,000 loan at $2,000 a month. Of that, around $500 is interest. The rest is principal.

Every month, $2,000 leaves the account. But only $500 shows up as an expense on the income statement. So the P&L looks cleaner than the actual cash position. And founders who only check their income statement never see it coming.

None of this means the business is in trouble. That's the part that makes it confusing.

Sales can be steady, margins can hold, and you can even be growing. But if cash is tied up in receivables, inventory, or loan repayments, you still feel it. I've watched founders spend months trying to fix their revenue when the real issue was just timing.

If a large share of your revenue is tied up in unpaid invoices, track your Days Sales Outstanding (DSO). A DSO above 45 days is generally considered a warning sign, though this varies by industry, even if your P&L looks strong

Revenue vs. profit vs. cash flow: how all three connect

Most founders consider these three variations of the same number. They're not. All of them measure something different, and they can move in opposite directions during the same month.

Now imagine that same coffee shop upgrades its espresso machine for $15,000. Operating cash came in at $10,000, but the equipment purchase pulled it down to -$5,000 for the month.

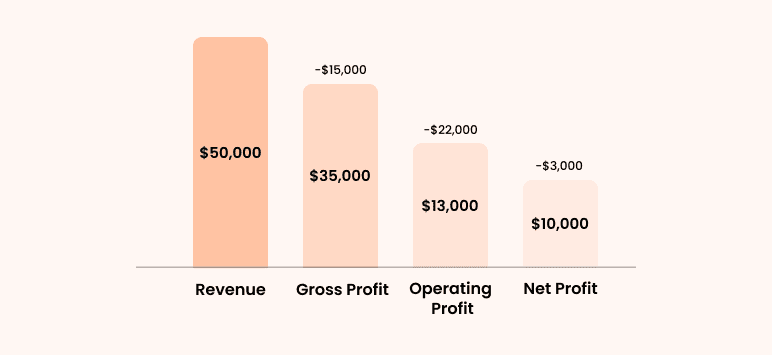

| Metric | What it means | Where it shows up | Example |

|---|---|---|---|

| Revenue | Total sales before any costs | Top of the income statement | $50,000 |

| Profit | What’s left after expenses | Bottom of the income statement | $10,000 |

| Equipment purchase | Investing cash outflow | Cash flow statement | -$15,000 |

| Cash flow | Actual money in your bank | Cash flow statement | -$5,000 |

I've shown this table to founders who couldn't believe all three numbers came from the same period. But it happens regularly.

Knowing which number to look at is equally important. I check the revenue to see if sales are working. I look at profit to see if pricing and costs hold up. I look at cash flow to know if the business can operate next week. Each one answers a different question, and leaning on just one gives you a false read.

Which one matters more: Cash flow or profit?

Cash flow keeps you operating. Profit keeps you viable. Founders lose sleep over profit margins in year one when the real threat was sitting in their bank account.

In the early days, cash flow is what determines whether you're still in business next month. Most startups run at a loss early on, and that's normal. What isn't survivable is running out of cash. The moment that happens, it's over, regardless of what the projections say.

Profit becomes the more pressing signal once the business is stable and self-funding. The question shifts from “can we keep operating,” to “is this worth continuing?” A company that does not even make a profit is either relying on external resources or living on borrowed time.

The position I see rattling founders most is when both cash flow and profit go negative at the same time. When that happens, there are usually three immediate steps:

● Cut costs immediately

● Collect outstanding invoices faster

● Bring in outside capital

Waiting to see which one improves on its own is rarely the right call.

When building financial projections for a business plan, always include a separate cash flow forecast alongside your income statement. Showing both signals that you understand how money actually moves through your business.

Most founders know they have a cash flow problem, but they don't have a system to catch it early enough to do something about it. So let’s understand how to track and improve them both.

How to track and improve both in your business

Start with cash flow, because that’s where problems show up first.

Get paid faster

If you're offering net-60 terms, push for net-30 where possible. Some businesses offer a 2% discount for payments within 10 days. It costs a little, but it keeps cash moving consistently instead of sitting in receivables.

Watch when money goes out, not just how much

Review expenses monthly with timing in mind. Delaying a non-critical payment by even a week can reduce pressure when cash is tight. Small shifts in timing add up.

Build a buffer

A 3-month cash reserve is the target I give most early-stage founders. If your business spends $15,000 a month, that's $45,000 set aside over time.

Forecast before problems appear

A cash flow forecast lets you see gaps before they become emergencies. Map expected inflows, planned expenses, and flag the months where cash looks thin.

Both SCORE and the SBA guidance on managing business finances offer free templates and resources if you're starting from scratch.

On the profit side:

Review gross margins monthly

A gross margin below 40% in most service businesses or below 50% in SaaS is worth investigating. If it's slipping month over month, pricing is usually the culprit, not costs.

Renegotiate supplier costs annually

Ask for volume discounts, extended payment terms, or annual pricing locks. Even a 5% reduction in COGS on $200,000 in annual purchases saves $10,000 straight off the bottom line.

Cut underperforming products or services

If a product or service runs below your average gross margin, it's dragging the overall number down. Flag anything below 20% gross margin as a candidate for repricing or removal.

When you are tracking both cash flow and profit in your business, make sure you avoid these mistakes:

- Send invoices immediately. Waiting even a few days pushes your cash collection further out.

- Separate personal and business accounts. Combining them makes accurate cash flow tracking nearly impossible.

- Review finances weekly. Waiting until the month-end means the problem has usually already cost you.

How cash flow and profit show up in your business plan

Something I always tell founders before they submit a plan: Lenders don't read financials the way you wrote them.

Most founders build their income statement first and treat the cash flow forecast as an afterthought. Lenders do the opposite. The first thing they check is whether the business has enough cash to operate. The profit story comes second.

Here's how each one actually gets used.

How does your income statement get read?

Your income statement projection usually runs a 3-year business plan. This is where investors spend time. They want to see if margins hold up, if revenue grows faster than expenses, and whether the model gets stronger over time or starts to strain.

How does your cash flow forecast get read?

The financial projections for your business plan should include a cash flow forecast covering 12 to 18 months, broken down monthly.

This is where lenders focus. They want to know if you can cover rent, payroll, and loan repayments in month four. I've seen plans where the business looked profitable by month three on paper, but cash went negative in month two because payments hadn't come in yet.

That one detail changes how the whole plan gets evaluated.

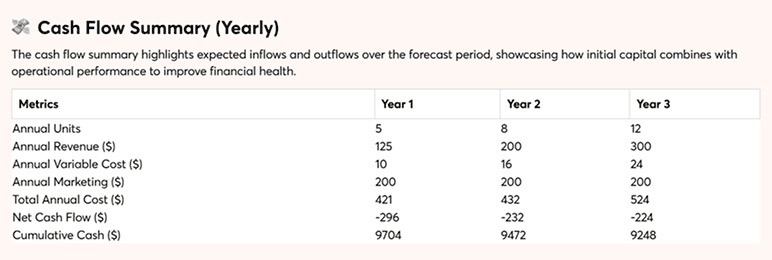

Created via Bizplanr financial model generator

Where most plans fall short

Most plans I've seen have the numbers. The income statement shows profit, but the cash flow forecast needs to show when that profit actually hits your account. If those two don't line up, lenders notice the gap without saying a word about it. Getting your business plan assumptions documented clearly is what keeps both statements honest.

When presenting projections, include three scenarios: conservative, moderate, and optimistic. Pay attention to how cash flow shifts across each one, not just profit. That's what tells a lender you've thought through the risks, not just the upside.

Conclusion

If there's one thing I'd want you to take away from this, it's that a profitable month and a healthy bank account are not the same thing. The sooner that clicks, the better you'll read your own business.

Most early-stage founders I've worked with weren't making bad decisions. They were just working off one number when they needed two. Profit tells you if the model works. Cash flow tells you if you can still operate while it does.

Build both into your plan from day one. If you're not sure where to start, Bizplanr's Financial Forecasting feature creates your income statement and cash flow forecast together, so nothing gets missed. For everything else that goes into wrapping up your plan, understanding how a marketing plan vs business plan differs, and reading the business plan conclusion guide are good next steps.

Your numbers are already there. You just need to know which ones to look at.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

What is the difference between cash flow and profit?

Profit is what's left after you subtract expenses from revenue, recorded when revenue is earned. Cash flow is the actual money moving in and out of your account, tracked when money actually changes hands. The gap between those two timelines is where most of the confusion starts.

Can a business be profitable but have negative cash flow?

Yes, and it happens more often than most founders expect. A consulting firm that invoices $30,000 in March but collects on net-60 will show a profit while running on empty for two months. The same goes for any business where loan principal repayments reduce cash without showing up as an expense on the P&L.

Is a P&L statement the same as a cash flow statement?

No. Your P&L shows revenue minus expenses to calculate profit. Your cash flow statement deals with actual money flow, including items that never show up on a P&L—loan repayments, equipment purchase, and owner draw.

Which is more important for a small business—cash flow or profit?

In year one, cash flow. Running at a loss early on is survivable. Running out of cash is not. Once the business is stable and self-funding, profit becomes a more important signal because it tells you whether the model actually works long-term.

How do cash flow and profit show up in a business plan?

Your business plan's financial section needs both. The income statement projection, usually covering 3 to 5 years, shows investors whether the business model is viable over time. The cash flow forecast, typically 12 to 18 months broken down monthly, shows lenders whether you can meet obligations when they come due.

Follow Kaylee Philbrick-Theuerkauf