You're putting together your first business plan, things are going fine, and then you get to the financial projections section. And you just... stop.

What are you supposed to forecast? Based on what?

Because you're a new business with no revenue history, no past data, nothing to base the numbers on. Honestly, this makes sense.

And I've watched dozens of first-time entrepreneurs get stuck at this step.

But here's what I want you to know. Every startup that has ever presented projections to a bank or an investor built them without historical data. Every single one. Well, it's the nature of starting something new.

Your numbers aren't a record of what happened. They're a reasoned case for what's possible. That's exactly what this guide covers: How to do that, step by step. Let's get into it.

Can you “actually” create a financial forecast without historical data?

Absolutely. It's simpler than most people expect. Without past sales data, you're not forecasting blind. You start with assumptions and make them as informed as possible.

For that, you need a few key things: Industry benchmarks for costs and margins, competitor pricing for what customers will pay, and a realistic estimate of your early customers.

Using those inputs, you can build your sales forecast, expense budget, and cash flow projection. This gives a complete picture of your finances, and every number has a clear reason behind it. That's what lenders actually look for.

5 Financial documents your startup needs (even without historical data)

Most first-time entrepreneurs think a financial forecast is just a revenue spreadsheet. In reality, a complete financial forecast covers five documents, showing a different side of your business finances.

Here's what they are:

- Sales forecast (what you'll earn)

- Expense budget (what you'll spend)

- Cash flow projection (what you'll have in the bank)

- Income statement (whether you'll be profitable)

- Balance sheet (what you own and owe)

You don't need to build all five from scratch. Once your sales forecast and expense budget are done, the other three largely build themselves. And before you start, it’s worth knowing:

How far out should your startup financial forecast go?

Most business owners create financial projections anywhere from 3 to 7 years, depending on their goals and industry. But 3 years is the most widely accepted standard. But lenders, especially SBA lenders, still expect a full 5-year view.

Anything beyond that, and your numbers start losing credibility because of too many unknowns far out.

Now that you know what you are building toward, let us start with the foundation.

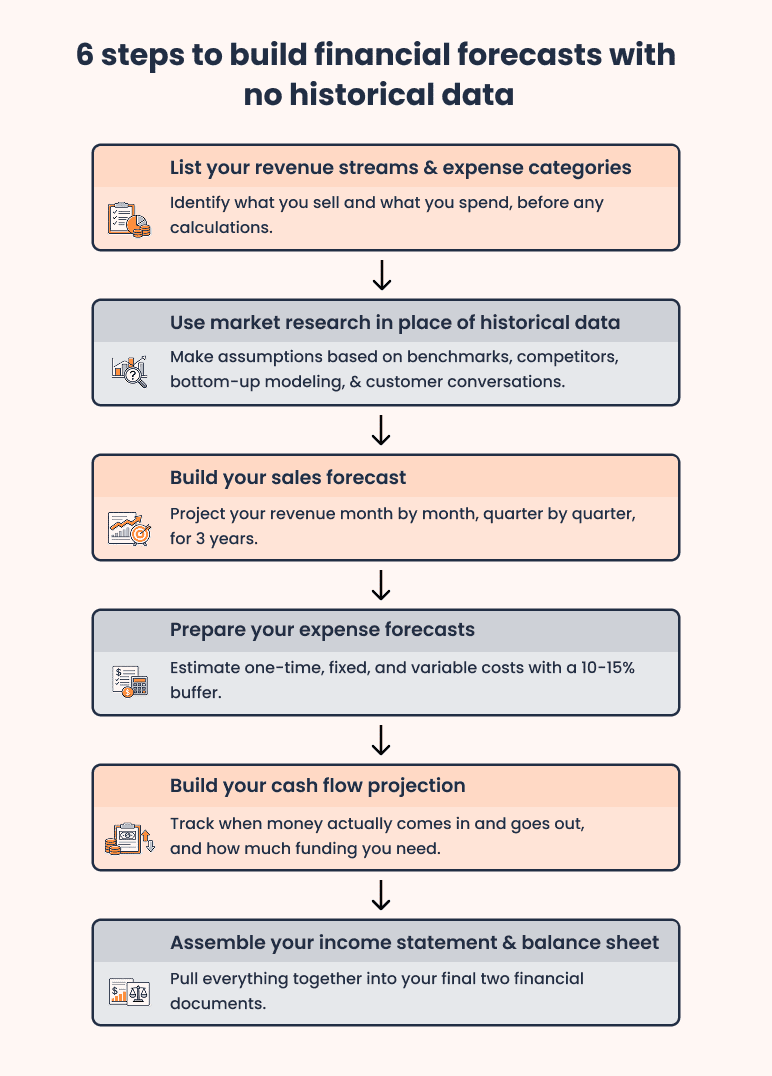

6 Steps to build financial forecasts with no historical data

Step 1: List your revenue streams and expense categories

Before you start crunching numbers, take 20 minutes to list out your revenue streams and expense categories. It'll save you hours of rework later.

Think what you sell in categories, not individual products. A bakery doesn't list every item on its menu separately. It simply groups everything into "baked goods," "custom cakes," and "catering."

Aim for 3 to 6 categories. Too many lines make the model hard to manage and harder for anyone reviewing it to follow.

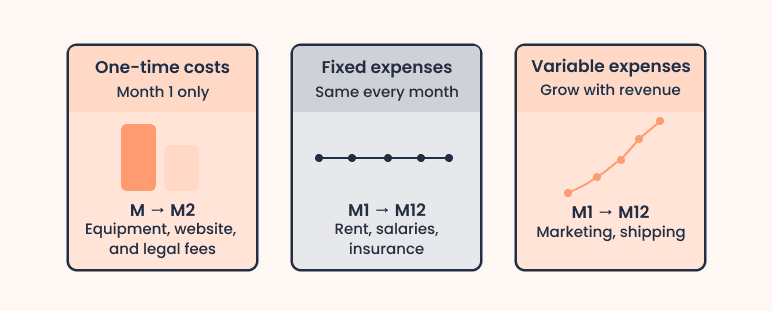

Then list your expenses. There are three types you need to account for:

- One-time startup costs, including equipment, website, and legal fees. These go in Month 1 only.

- Fixed expenses, such as rent, salaries, and insurance. Same amount every month, no matter what.

- Variable expenses, like marketing, materials, and shipping. These go up as your sales go up.

The same grouping logic applies to expenses. If you have electricity, internet, and a water bill, group them under "utilities" rather than listing each one separately.

Don't try to tackle everything at once. Pick one category, work through it completely, then move to the next.

Should I include costs I'm not sure about yet, or leave them out?

Not adding potential costs could be the wrong move. A rough estimate, even an imperfect one, is always better than a blank row. If you're unsure about costs, look up local rates or use industry benchmarks as a starting point.

Leaving costs out makes your forecast look more profitable than it really will be, and tells a lender you haven't thought the business through fully.

These are just educated estimates, not perfect predictions. You will revisit and adjust them as you go. Getting the categories right at this stage is what matters most. The precision comes later.

If you’re not sure what categories apply to your specific business, Bizplanr's AI Assistant can help you figure that out before you start forecasting numbers.

Step 2: Use market research in place of historical data

You don't have historical data, but that doesn't mean you're forecasting blind. There are four sources I always recommend to first-time founders when building key financial assumptions from scratch.

1. Industry benchmarks

Every industry has standard numbers. Average profit margins, typical cost ratios, and common pricing ranges.

- The SBA.gov publishes benchmark data for common business types.

- IBISWorld and Statista are also reliable sources for industry-level financials.

- Trade associations in your vertical often publish annual reports with even more specific numbers.

A restaurant, for example, should target food costs at 28 to 35% of revenue. That's a widely accepted benchmark you can plug straight into your forecast as a starting assumption. But…

What if I can't find industry benchmarks for my specific niche?

Broaden your research and look at the closest industry you fall under. Use those numbers. A virtual fitness coach, for example, won't find benchmarks labeled "virtual fitness coaching."

However, the broader health and wellness industry has plenty of published data on cost ratios, pricing ranges, and profit margins that translate reasonably well. It won't be a perfect match, but it's close enough to build from.

The key is to be transparent about this when you present your numbers.

2. Competitor research

Once you have benchmarks, look at what similar businesses charge. That's your clearest signal for what customers are willing to pay. You can also:

- Study their pricing

- Read founder interviews

- Check job postings for team size & payroll

If a competitor is a public company, their annual reports and 10-K filings (freely available on SEC.gov) have more financial detail than most people realize.

Here’s a common concern I hear from first-time entrepreneurs whose business is unique:

What if I don't have direct competitors?

I would say: If direct competitors are hard to find, don't let this stop you, though. Look for indirect ones, businesses serving the same customer with a different solution. Their pricing still gives you the same useful signals.

For example, a meal kit delivery service doesn't directly compete with a grocery store. But studying grocery pricing and margins tells you a lot about what customers are willing to spend on food.

You don't need a perfect apples-to-apples comparison to build a forecast.

3. Bottom-up sales modeling

This is the forecasting model I'd recommend over anything else, especially if you're presenting to investors.

Instead of saying "we'll capture 1% of a $10 million market," start with your own realistic activity. Say you can make 50 sales calls a week, convert 10% of them, and your average deal is $1,200. That's $6,000 a week in potential revenue.

And it’s a number you can actually defend. Build your revenue estimate from such real inputs.

4. Customer validation data

Use your personal network, local business groups, or LinkedIn to reach out to 10-20 potential customers before you forecast. And ask:

- What they’re willing to pay

- How often they'd buy

- What problem they're trying to solve

Pre-orders, waitlist signups, or a simple letter of intent all count as data.

Honestly, one customer saying "I'd pay $X for this" is worth more than any market report. It's also exactly what lenders and investors want to see.

How many customer interviews are "enough" to call it data?

Ten to fifteen conversations are genuinely enough. If the first ten people describe the same problem and agree on a similar price point, that's a reliable signal. It won't be perfect, and it doesn't need to be.

Don't wait for fifty interviews to start building. What matters is that your assumptions are grounded in real conversations rather than guesswork.

It's the difference between a forecast a lender trusts and one they quietly dismiss.

Here's a quick summary for all four sources:

| Source | What you can get | Credibility with lenders |

|---|---|---|

| Industry benchmarks | Cost ratios, margins, pricing ranges | High |

| Competitor research | Pricing signals, cost structure | Medium-high |

| Bottom-up modeling | Realistic revenue estimate | High |

| Customer conversations | Willingness to pay, demand signals | Very High |

None of these sources will give you perfect numbers. That's okay. What they give you is a logical, research-backed foundation, and that's what lenders and investors are actually looking for.

Step 3: Build your sales forecast

With your research in hand, it's time to build the sales forecast. It’s the most important aspect of your startup financial plan. Everything else, your expenses, cash flow, and profitability, flows directly from your sales forecast.

Get this right, and the rest becomes significantly easier.

For Year 1, build your sales forecast month by month. Years 2 and 3 can be shown quarterly. Most lenders and investors want a 3-year view, and this format gives them exactly that.

The formula depends on your business type. But the logic is the same: Start with how many customers or units you can realistically reach, multiply by your price, and that's your monthly revenue.

- Product business: Units sold × price per unit = revenue

- Service business: Number of clients × average monthly fee = revenue

- SaaS: (new customers + retained customers) × monthly price = MRR (monthly recurring revenue)

Don't forget to consider churn for service and SaaS businesses. Not every customer from Month 1 will still be with you in Month 6.

Your first few months will be slow, and that's completely normal. But most first-timers get ramp-up wrong. They overestimate how fast sales come in early on. Start slow and build gradually. Be conservative.

A forecast that grows slowly but logically is far more believable than one that jumps to big numbers right away.

Let’s take an example of a SaaS startup charging $99 per month. Here's what a realistic 12-month sales forecast looks like:

| Month | New customers | Churned | Total customers | Price | Revenue |

|---|---|---|---|---|---|

| 1 | 5 | 0 | 5 | $99 | $495 |

| 2 | 8 | 0 | 13 | $99 | $1,287 |

| 3 | 9 | 2 | 20 | $99 | $1,980 |

| 4 | 12 | 2 | 30 | $99 | $2,970 |

| 5 | 15 | 2 | 43 | $99 | $4,257 |

| 6 | 32 | 0 | 75 | $99 | $7,425 |

| 7 | 20 | 5 | 90 | $99 | $8,910 |

| 8 | 22 | 4 | 108 | $99 | $10,692 |

| 9 | 25 | 5 | 128 | $99 | $12,672 |

| 10 | 22 | 5 | 145 | $99 | $14,355 |

| 11 | 28 | 5 | 168 | $99 | $16,632 |

| 12 | 32 | 0 | 200 | $99 | $19,800 |

(*Churn varies month to month in early-stage businesses. In the early months, it's lower simply because there are fewer customers to lose. As your base grows, it becomes a more meaningful number to track.)

See how growth begins slowly and builds gradually. That's exactly what a credible forecast looks like. Month 1 has just 5 customers. By Month 12, that's grown to 200. Logical, gradual, and easy to defend.

A forecast that shows 200 customers in Month 1 raises immediate questions. One that shows a logical ramp tells a believable story.

One thing to note here: When your business sells physical products, take one extra step.

Subtract your cost of goods sold from revenue to get your gross profit. This shows lenders or investors how much your business actually keeps after delivering the product.

How conservative is too conservative? Can I scare off investors by going too low?

Being conservative actually builds credibility.

Investors know that first-year revenue almost always comes in lower than expected. What they're looking for is whether your numbers make logical sense, not whether they're impressive.

Just make sure your financial projections are realistic enough to show your business can survive the early months. If your conservative case shows you running out of money in Month 3, that's the real issue to address.

Step 4: Prepare your expense forecasts

You already have your expense categories from Step 1. Now it's time to put actual numbers against them.

And the good news: Expenses are easier to estimate than revenue. Most of them are fixed, meaning you know exactly what they'll cost before you even make a single sale.

Work through one category at a time. Start with your one-time startup costs, then fixed monthly expenses, then variable ones.

How do I estimate costs for things I've never paid for before (like commercial rent or insurance)?

The honest answer is you don't need a perfect number at this stage. You need a defensible one.

Start with a Google search for local rates in your city. Commercial rent, insurance premiums, and professional fees all vary by location, so local numbers will always be more accurate.

The Bureau of Labor Statistics is also worth checking for industry-level cost benchmarks. And if you're still unsure, just get a real quote from an insurance broker or a local landlord.

For unexpected costs, add a 10 to 15% buffer on top of your total monthly expenses.

Every new business hits surprises in Year 1. Software price increase, an unexpected repair, or a legal fee you didn't anticipate. Lenders expect to see this buffer in your forecast.

And don't forget your own salary, even if it's $0 right now. Pick a specific month when your revenue can realistically support it. Most founders begin paying themselves somewhere between Month 6 and Month 12.

Here's a simple example of a first-year expense budget for a small SaaS startup:

| Expense | Type | Month 1 | Month 2-6 | Month 7-12 |

|---|---|---|---|---|

| Website development | One-time | $3,000 | $0 | $0 |

| Legal & incorporation | One-time | $1,500 | $0 | $0 |

| Rent | Fixed | $1,200 | $1,200 | $1,200 |

| Salaries | Fixed | $4,000 | $4,000 | $5,000 |

| Insurance | Fixed | $200 | $200 | $200 |

| Marketing | Variable | $500 | $800 | $1,500 |

| Software subscriptions | Fixed | $300 | $300 | $300 |

| Owner salary | Fixed | $0 | $0 | $2,000 |

| Miscellaneous buffer | Buffer | $960 | $650 | $1,020 |

Step 5: Build your cash flow projection

Most new business owners focus entirely on revenue. How much will I make? When will I be profitable? Those are important questions. But there's an equally important question most people miss:

Will I have enough cash in the bank to pay my bills while I'm waiting for revenue to grow?

That's exactly what a cash flow projection answers.

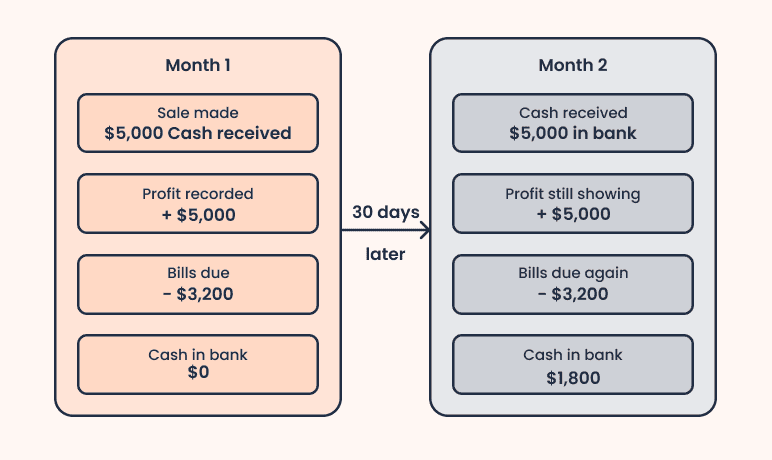

First, understand that profit and cash are not the same thing. Profit is what your income statement shows. Cash is what's actually in your bank account.

Let’s say you make a $5,000 sale in January, but your customer pays in February based on net-30 terms. You've earned that money, but you won't see it for 30 days. Your bank account in January is empty. Your bills don't wait 30 days.

That gap is what cash flow tracks before it becomes a problem.

To build a cash flow projection, take your sales forecast from Step 3 and note when you actually expect to receive each payment. Then take your expenses from Step 4 and note when each bill is due.

The difference between those two each month is your net cash. Add it up cumulatively, and you can see exactly when your business runs out of money and when it stops needing outside support.

Here's what it looks like using the SaaS example from Step 3:

| Month | Cash In | Cash Out | Net Cash | Cumulative Balance |

|---|---|---|---|---|

| 1 | $495 | $11,900 | -$11,405 | -$11,405 |

| 2 | $1,287 | $7,500 | -$6,213 | -$17,618 |

| 3 | $1,980 | $7,500 | -$5,520 | -$23,138 |

| 4 | $2,970 | $7,800 | -$4,830 | -$27,968 |

| 5 | $4,257 | $7,800 | -$3,543 | -$31,511 |

| 6 | $7,425 | $8,100 | -$675 | -$32,186 |

| 7 | $8,910 | $8,100 | $810 | -$31,376 |

Month 7 is where net cash finally turns positive. Up until that point, the business is spending more than it's bringing in every single month. It means you will need to fund those early months through a loan, an investor, or your own savings.

How do I figure out how much funding I actually need from this?

Your cumulative balance column answers that directly. Find the lowest number in it. That's your maximum cash gap, the point where your business needs the most outside support before revenue takes over.

Once you have that figure, add 10 to 15% on top as a buffer for unexpected delays or slower growth. That final number is your realistic funding target, and you can defend every dollar of it with the projections you've already built.

Most SBA lenders and investors want to see 12 to 24 months of monthly cash flow projections, so build yours out that far.

Step 6: Assemble your income statement and balance sheet

Once you have completed Steps 1 through 5, most of your work is already done. Now, you just need to pull the numbers together into two final documents.

The income statement (P&L)

This is the simplest of the two. You already have everything you need from your sales forecast and expense budget. The formula is straightforward:

Revenue - Cost of goods sold = Gross profit

Gross profit - Operating expenses = Operating income

Operating income - Taxes and interest = Net income

For Year 1, show this monthly. For Years 2 and 3, an annual summary is enough. Here's what a Year 1 income statement looks like:

| Category | Month 1 | Month 3 | Month 6 | Month 12 |

|---|---|---|---|---|

| Revenue | $495 | $1,980 | $7,425 | $19,800 |

| COGS | $0 | $0 | $0 | $0 |

| Gross Profit | $495 | $1,980 | $7,425 | $19,800 |

| Operating Expenses | $11,900 | $7,500 | $8,100 | $8,100 |

| Operating Income | -$11,405 | -$5,520 | -$675 | $11,700 |

| Interest Expense | $0 | $0 | $0 | $0 |

| Tax (25%) | $0 | $0 | $0 | $2,925 |

| Net Income | -$11,405 | -$5,520 | -$675 | $8,775 |

The balance sheet

The balance sheet is a snapshot of where your business stands financially at a specific point in time. It works off one simple equation:

Assets = Liabilities + Owner's equity

Your assets are the cash you've put in, any equipment you've purchased, and any inventory you're holding. Your liabilities are any loans or credit you've taken on to get started. The difference between the two is your owner's equity.

Do I really need a balance sheet if I'm pre-revenue?

Yes. Most SBA loan applications and investor decks require one.

It doesn't need to be complicated. Even a simple one with just a few line items tells a lender everything they need to know about where your business stands right now.

And if right now your only asset is the cash you've put in, that's completely fine. It's actually the most common situation for a pre-revenue startup.

A balance sheet that shows your startup cash as an asset, a loan as a liability, and the difference as owner's equity is a valid, complete document. That’s what most lenders expect to see at this early stage.

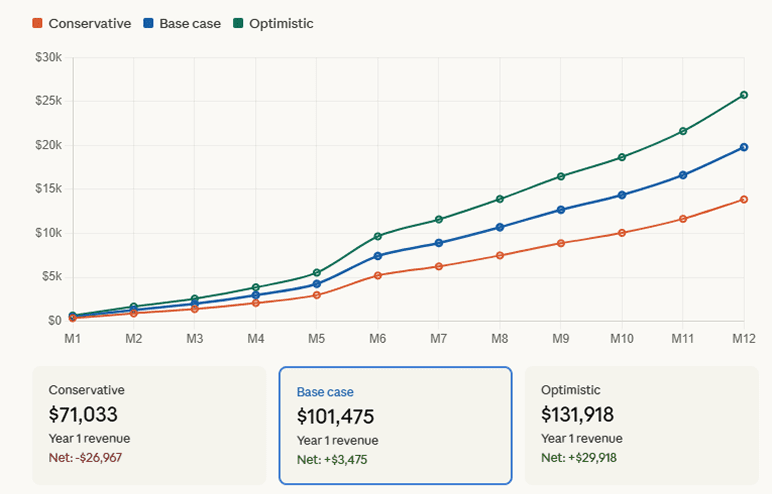

Model three scenarios (base, best, worst case)

If you show up to a lender or investor meeting with a single set of projections, the first thing they'll ask is: "What if things don't go as planned?"

Presenting three scenarios tells them you've thought about that already. It's one of the simplest ways to build credibility before anyone asks a question. Here's exactly how to do it:

1. Conservative scenario

Cut your revenue projections by 30 to 40% from your base case. Keep your expenses exactly the same. This answers the question: what happens if customers take longer to come than expected?

It's the scenario every lender is quietly running in their head when they review your numbers.

2. Base case scenario

This is your most likely outcome, built from the market research and assumptions you gathered in Step 2. Not overly optimistic, not worst case. Just your honest best estimate of how things will go.

3. Optimistic scenario

Increase your revenue by 30 to 40% from your base case. Keep expenses the same or adjust slightly upward for growth-related costs.

But think about what would actually need to happen for this to be true. Faster word of mouth? A big partnership? Be specific. Optimism without a reason behind it isn't convincing to anyone.

Here’s how to present so anyone reviewing your business plan can compare all three instantly:

| Category | Conservative | Base Case | Optimistic |

|---|---|---|---|

| Year 1 Revenue | $71,033 | $101,475 | $131,918 |

| Year 1 Expenses | $98,000 | $98,000 | $102,000 |

| Net Income | -$26,967 | $3,475 | $29,918 |

| Break-even Month | Month 14 | Month 10 | Month 8 |

Remember that the gap between your conservative and optimistic numbers should feel believable.

If your conservative case shows $100,000 and your optimistic case shows $5 million, the whole forecast loses credibility. Keep the spread tight and logical.

Build your financial forecast using Bizplanr

Now that you've worked through all six steps, you know exactly what goes into a financial forecast.

Honestly, keeping all of it consistent in a spreadsheet is no small task. Change one assumption, and suddenly, numbers are off across multiple documents.

That's where Bizplanr's financial model generator makes a real difference. It gives you a solid, realistic forecast without the back-and-forth of building everything manually. Even, no formatting, no numbers falling out of sync.

And if you want to model your conservative, base, and optimistic scenarios side by side, our AI financial forecasting software lets you do that without starting from scratch.

You've done the hard work of understanding what goes into a forecast. Bizplanr just helps you build it faster.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

How do you create a financial forecast with no historical data?

You replace the historical data with research. Here's the basic order to follow:

- List your revenue streams and expense categories

- Use industry benchmarks and competitor research to set your assumptions

- Build your sales forecast first

- Add your expense budget

- Assemble your cash flow projection, income statement, and balance sheet

- Model three scenarios: conservative, base, and optimistic

That's it. No historical data needed, just research and logical assumptions.

How far out should a startup financial forecast cover?

Three years is the standard. Year 1 monthly, Years 2 and 3 quarterly. If you're applying for an SBA loan or bank financing, plan financials for the full three years. Some early-stage investors will accept 18 months, but three years is the safest default.

What financial documents does a startup need for its business plan?

A complete startup financial forecast has five documents:

- Sales forecast

- Expense budget

- Cash flow projection

- Income statement (P&L)

- Balance sheet

Most lenders and investors want all five, with Year 1 broken down by month and Years 2 and 3 shown quarterly.

Is it OK if my startup's financial projections are wrong?

Yes, absolutely. And that's completely normal. No forecast is ever perfectly accurate, especially for a brand-new business. What matters is that your financial projections are based on real research and you can explain where they came from. Lenders and investors don't expect perfection. They expect logic.

What do investors look for in financial projections for startups?

Investors look for a few specific things:

- Realistic growth numbers, not overnight millions

- Clear, sourced assumptions behind every key figure

- Three scenarios showing you've thought about risk

- A cash flow projection showing when and how much funding is needed

- A path to profitability, even if it takes 12 to 18 months to get there

Follow Kaylee Philbrick-Theuerkauf