If you've ever looked at a cash flow statement and wondered why your accountant started with net income instead of actual cash, you've already stumbled onto the direct vs indirect method cash flow debate.

Both methods arrive at the same number. So if the result is identical, why does the method matter?

It comes down to what the statement shows you and who needs to read it. I'll walk you through the direct method cash flow vs indirect using the same example so you can see how they differ and choose the one that's right for you.

What is a cash flow statement (and why does the method matter)

A cash flow statement tracks how money actually moves in and out of your business over a period of time. Not profit on paper, but real cash received and paid. It answers the question your income statement can't: where did the cash go?

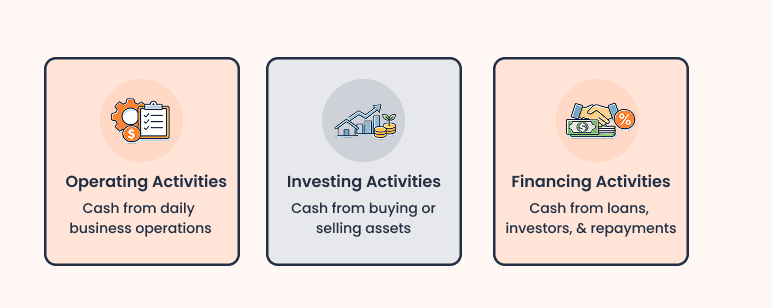

It's broken into three sections:

The direct vs. indirect method only affects the operating activities section. The investing and financing sections are prepared the same way regardless of which method you choose. So you're not picking between two completely different statements. You're choosing how to calculate and present just one section.

The operating section is where your business either shows real cash strength or exposes a problem. That's the one you're deciding about.

The direct method: how it works (with example)

The direct method builds your operating cash flow from actual cash activity. You record every dollar collected from customers, and every dollar paid out to run the business. There's no working backward from profit or non-cash adjustments.

Let’s see how it works in practice:

- Start with cash received from customers. This is the total cash collected from sales during the period, not what you invoiced.

- Subtract cash paid to suppliers. Payments are made for inventory, raw materials, or services purchased.

- Subtract cash paid to employees. Wages, salaries, and payroll-related payments.

- Subtract other operating payments. Rent, utilities, marketing, and other day-to-day expenses.

To see how this plays out with real numbers, take a coffee shop that's six months into operations:

| Item | Amount |

|---|---|

| Cash received from customers | $120,000 |

| Cash paid to suppliers | ($45,000) |

| Cash paid to employees | ($35,000) |

| Rent and utilities | ($15,000) |

| Other operating expenses | ($5,000) |

| Net cash from operations | $20,000 |

Every line is a real cash transaction. Nothing is estimated or derived from another statement. That's what makes this method easy to read but harder to prepare.

That clarity comes with some real trade-offs, though.

- You get a clear view of where cash is coming in and going out, with no adjustments to interpret.

- It's easy to read even if the person reviewing your financials isn't an accountant.

- FASB, the body that sets U.S. accounting standards, encourages this method for its clarity.

However, there are some downsides to it:

- You have to monitor every single transaction of cash, which becomes time-consuming as your business expands.

- The default setting of most accounting software is the indirect method, and it may take additional effort to produce this form.

- It is used by only about 2% of companies, and lenders and investors are less familiar with it.

When you want to use the direct method, begin with 30 days of your bank transactions and split them into four categories: customer receipts, supplier payments, payroll, and other expenses. If you can categorize everything cleanly in under an hour, this method is practical for your business.

The indirect method: how it works (with example)

The indirect method takes a different approach. Rather than updating all the cash transactions, it begins with your net income and works backward, with a series of adjustments until you arrive at the real cash that your business produced.

With an income statement and a balance sheet already in place, most of the figures you require are already in these statements. This is what makes this method quicker to prepare.

Let’s see how it work:

- Start with net income. This comes directly from your income statement.

- Add back non-cash expenses. Depreciation and amortization reduce your profit on paper but don't involve actual cash leaving the business, so you add them back.

- Adjust for gains or losses. Remove any gains from selling assets since that profit above book value gets classified under investing activities, not operations.

- Account for working capital changes. This is where most of the adjustment happens:

- Increase in accounts receivable → subtract (cash not yet collected)

- Increase in inventory → subtract (cash spent but not yet sold)

- Increase in accounts payable → add (expenses recorded but not yet paid)

These changes are driven by your cash flow assumptions, so make sure they're grounded in realistic numbers.

Using the same coffee shop from the direct method example, this is what the indirect method looks like:

| Item | Amount |

|---|---|

| Net income | $19,000 |

| Add: Depreciation | $5,000 |

| Increase in accounts receivable | ($3,000) |

| Increase in inventory | ($4,000) |

| Increase in accounts payable | $3,000 |

| Net cash from operations | $20,000 |

The result is $20,000, the same number the direct method produced. Both methods are calculating the same thing, just from opposite directions. The direct method shows you the cash transactions themselves. The indirect method shows you how profit converts into cash.

That distinction shapes both what this method does well and where it falls short.

Advantages:

- It's faster to prepare because you're working from financial statements you've already built.

- It works naturally with accrual accounting, which is how most businesses already track their finances.

- Lenders, investors, and accountants are comfortable reading it since it is used by about 98% of companies.

- It demonstrates how your profit is linked to your real position of cash and is helpful background information to someone analyzing your financials.

Disadvantages:

- It doesn't show individual cash inflows and outflows, and therefore, it is more difficult to identify the exact source of cash inflows or cash outflows.

- If you are not familiar with accrual accounting, the adjustments can be hard to follow.

If you are using QuickBooks or Xero, go to your reports and find the cash flow statement. By default, it will be in indirect form, which means you might already have this ready without knowing it.

Direct vs. indirect: key differences at a glance

The distinctions between the two approaches boil down to a few important aspects.

| Basis | Direct method | Indirect method |

|---|---|---|

| Starting point | Actual cash received and paid | Net income (profit) |

| What it shows | Real cash inflows and outflows from operations | How profit is adjusted to arrive at cash flow |

| Preparation effort | High, requires tracking every cash transaction | Lower, uses existing income statement and balance sheet |

| Who uses it | Rare, around 2% of companies | Standard, around 98% of companies |

| Best for | Small businesses, internal cash tracking | Reporting, business plans, investors |

| GAAP treatment | Preferred for clarity but rarely used in practice | Accepted and most commonly used |

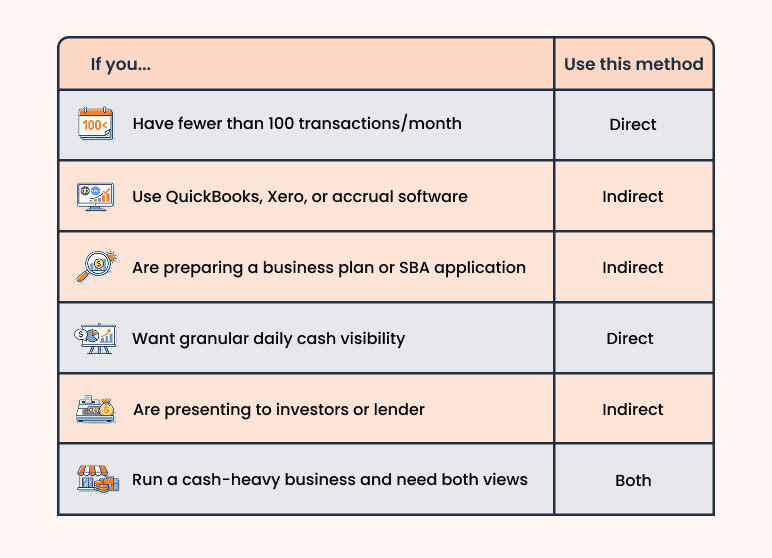

How to choose the right method for your business

The answer comes down to four things:

1) Your transaction volume

If you are processing roughly 100 or fewer transactions a month, the direct method is manageable. You can track every cash inflow and outflow without it becoming a burden. Once you scale past that, I'd recommend switching to indirect. The manual tracking required for the direct method gets time-consuming fast.

2) Your audience

Think about who's sitting on the other side of the table. Investors and lenders are comfortable with the indirect method because that's what they see from almost every business they review. Some lenders may ask for the direct method if they want a more granular view of cash activity, so it's worth confirming before you finalize your format.

3) Your accounting system

If you're using QuickBooks or Xero, the indirect method is already built into how your reports are generated. Switching to direct means additional manual tracking on top of your existing setup. If you're on a simple cash-basis system, direct may actually be easier to produce.

4) Your purpose

For day-to-day cash tracking and internal visibility, the direct method gives you a sharper picture. For formal reporting, business plans, and investor presentations, indirect is the standard. Most of those plans include 3-year financial projections, and the indirect method is what keeps everything consistent across all three statements.

Here's a quick reference to pull it all together:

Which cash flow method works best in a business plan?

If you're building a business plan for a bank loan, SBA funding, or investors, my recommendation is to use the indirect method. This isn't just a preference. It's what banks, SBA lenders, and investors expect to see. If you're still working on the structure, here's how to format your business plan before adding financial projections.

The indirect method connects directly to your projected income statement and balance sheet, so everything ties together cleanly, and your numbers are easier to review and validate.

However, FASB under U.S. GAAP encourages the direct method for its clarity. IFRS takes a similar position. But in practice, the indirect method became the standard because it's faster to prepare and fits naturally with how most businesses track their finances. That gap between what's preferred on paper and what's actually used is worth knowing before you decide.

There are cases where including both methods makes sense. If you're running a cash-heavy business like a retail store or restaurant, adding a direct view alongside your indirect statement can help you track daily register receipts, supplier COD payments, and tip payouts separately. But for formal planning and reporting, the indirect method is what carries weight.

Structure your projections with monthly cash flow for Year 1 and annual totals for Years 2 and 3. This is the standard format for 3-year financial projections that banks and SBA lenders expect.

Common mistakes to avoid when preparing your cash flow statement

Even with the right method chosen, a few errors come up consistently. Let’s talk about a few:

1. Mixing cash-basis and accrual numbers

When you are using the indirect method, you must have everything flow out of your accrual-based income statement and balance sheet. It will not give accurate results to pull numbers out of a cash-basis system and tweak them under the indirect method. Choose one accounting basis and keep it.

For example, if your books are cash-basis but you're trying to apply indirect method adjustments, your working capital changes won't reflect reality. Pick one accounting basis and stay consistent.

2. Double-counting depreciation

The indirect method adds depreciation to the net income since it is a non-cash expense. One of the errors is adding it back and then also adding it as an individual cash outflow in another part of the statement. Once, it appears as an add-back, and that is all.

3. Forgetting working capital changes

One of the most frequent mistakes that I come across is the omission of the accounts receivable, inventory, and accounts payable adjustments. These adjustments have a direct impact on the extent to which your business actually made cash, despite your profit appearing to be running along.

Say your business made $20,000 in profit, but customers owe you $8,000 that hasn't been collected yet. Your actual cash from operations is $12,000, not $20,000. If your working capital section is blank, your number is almost certainly wrong.

4. Classifying asset sale proceeds as operating cash

If you sold a piece of equipment, those proceeds go under investing activities, not operations. Only the gain above book value gets removed from the operating section as an adjustment. Putting the full proceeds in operations overstates your operating cash flow.

5. Using invoiced revenue instead of cash collected

What you invoiced, not what you collected, is what you have on your income statement. The cash is not in your cash flow statement until a customer makes a payment to you. If you invoiced a client $5,000 in December but they paid in January, that $5,000 doesn't belong in your December cash flow statement. Only cash actually received counts.

Conclusion

The direct method shows you the actual cash transactions. The indirect method shows you how profit becomes cash. Both land on the same number, but what you see along the way is completely different.

For most small business owners, my recommendation is the indirect method. It's what lenders, SBA reviewers, and investors expect, and it keeps your financials consistent across all three statements.

Once you're ready to build your projections, you can use Bizplanr to structure your cash flow in the standard indirect format so your financial projections stay aligned from day one.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

What is the difference between the direct and indirect methods of cash flow?

The direct method records cash collected from customers and cash paid to suppliers, employees, and operating expenses. Every line is an actual cash transaction, nothing derived or adjusted.

The indirect method starts with net income and works backward, adjusting for non-cash items and working capital changes until it reflects real cash. Both produce the same operating cash flow number, but the direct method shows the transactions themselves, while the indirect method shows how profit converts into cash.

Do both methods produce the same operating cash flow number?

Yes, always. If your direct and indirect calculations produce different numbers, the issue is usually a misclassified transaction or a working capital adjustment that's been missed. Go back and check your accounts receivable, inventory, and accounts payable changes first. That's where most discrepancies hide.

Is direct or indirect cash flow easier to prepare?

The indirect method is easier for most businesses because you're working from financial statements you've already built. The direct method requires tracking every individual cash transaction separately, which is manageable at low volumes but gets time-consuming as your business grows. If you're using accounting software, indirect is almost certainly what your system generates by default.

Why do most companies use the indirect method?

It's faster and shows the relationship between profit and cash in a way that's useful for anyone reviewing your financials. Even when auditors request the direct method, most companies provide the indirect method with a supplemental direct-method schedule rather than switching formats entirely.

Which cash flow method should I use in a business plan?

Use the indirect method. It's the format banks, SBA lenders, and investors are used to reading, and it ties directly to your projected income statement and balance sheet. If you're running a cash-heavy business, consider adding a direct method view for internal tracking, but keep the indirect method as the primary format in your plan.

Follow Vinay Kevadiya