If you’re reading this, you likely have one of these confusions:

(1) Is the budget and forecast the same thing? (2) Okay, they’re different; so what’s the difference? Or, (3) Which one should I really care about?

If you’d accept a quick answer:

- Budget = a fixed financial plan created before a period starts

- Forecast = an estimate updated based on actual performance

You use the budget to measure gaps (variance) and take actions (cut costs, push sales), and the forecast to project where you’re actually heading and adjust decisions accordingly.

Still confused? Don’t worry, let’s discover the full difference between budget vs. forecast, when to use each, and how both fit into your business plan.

What is a budget?

Think of your budget as a spending plan you set at the start of the year, before anything actually happens. It’s not a guess about what might happen. It’s a decision about what you want to make happen.

A budget defines how much revenue you aim to generate and sets clear limits on how much you can spend. It puts boundaries around your financial decisions.

You’re not trying to predict the future here. You’re setting targets and defining the rules needed to reach them.

In simple terms, a budget is your financial blueprint. It lays out:

- Expected Revenue: The sales targets you must hit

- Planned expenses: The strict limits on what you can spend

- Target profit (profit goals): The financial goal you want to end up with

The majority of businesses prepare a budget annually, typically before the start of a new financial year. The business owner usually prepares it, though occasionally with assistance from an accountant or the finance department.

To get deeper insights, let’s understand with an example. Imagine you run a small coffee shop. At the start of the year, you estimate your numbers like this:

| Category | Annual Amount |

|---|---|

| Revenue | $180,000 |

| COGS | $60,000 |

| Operating Costs | $90,000 |

| Net Profit | $30,000 |

This is your definitive game plan. Your team knows they have to bring in $180,000 in sales, and they know they are not authorized to spend a single penny over $90,000 on operations.

But remember, this is just a plan. It doesn’t guarantee results. It simply sets the direction. A budget does not change easily once it’s set. It reflects what you planned at the start, not what’s happening right now.

If something shifts mid-year, like lower customer demand or rising costs, your budget still stays the same. You don’t rewrite it every time things change. Instead, you use it as a reference point to see how far off you are from your original targets.

And this is exactly where forecasting comes in.

Don’t overthink your first budget. Start with last year’s numbers or your best estimates. Adjust as you learn. A rough budget is always better than having none.

What is a financial forecast?

If a budget is your plan, a forecast is your reality check. A financial forecast shows where your business is likely heading based on actual performance and current trends. Unlike a budget, which sets targets in advance, a forecast updates those expectations using real data.

In simple terms, a budget is what you want to happen. A forecast is what’s likely to happen. Forecasts can be short-term (monthly, quarterly) or long-term (12 to 36 months out), depending on what decisions you're trying to make.

Let us go back to the coffee shop example to see how this works:

At the start of the year, you planned $180,000 in revenue. But by June, your actual sales are tracking 15% below your target. Based on this trend, you adjust your expectations.

That's not failure; that's useful information you can actually act on. Your updated forecast now looks like this:

| Metric | Amount |

|---|---|

| Budget | $180,000 |

| Forecast | $153,000 |

This shift helps you act early. You can adjust spending, rethink pricing, or push sales before the gap gets worse. You might cut costs, run promotions, or rethink pricing to stay on track. That’s the real value of forecasting. It helps you respond, not just plan.

Update your forecast at least quarterly. The more often you compare where you’re going against where you planned, the faster you can adjust your decisions.

Budget vs. forecast: Key differences at a glance

Now that you understand budgets and forecasts individually, let's learn more about the differences between budgeting and forecasting using the table below:

| Basis | Budget | Forecast |

|---|---|---|

| Purpose | Sets financial targets and spending limits | Predicts likely financial outcomes |

| Timeframe | Fixed period, usually 12 months | Short-term (monthly/quarterly) or long-term (1–3 years) |

| Update Frequency | Once a year, rarely revised | Regularly updated (monthly or quarterly) |

| Data Basis | Goals, assumptions, and strategic plans | Actual performance data and current trends used in your financial forecast |

| Flexibility | Relatively fixed once set | Adjusts as new information comes in |

| Detail Level | High detail across all expense categories | Varies, often focused on key revenue and cash flow drivers |

| Who Uses It | Owners, accountants, department heads | Owners, CFOs, investors, lenders |

| Key Focus in 2026 | Cost control, investor/loan compliance, and baseline performance measurement | Cash flow preservation, risk mitigation, and proactive pivots amid uncertainty |

| Modern Trend Integration | Often reviewed periodically and adjusted based on performance and cost changes | Increasingly uses AI/scenario tools for 25–30% more accurate combined planning |

Now, let’s break down the differences that actually impact your decisions.

1) Purpose: A budget sets your targets. For example, you decide to spend $50,000 on marketing this year. A forecast checks if that plan still makes sense based on actual results.

2) The data source: A budget is built on assumptions. A forecast uses real numbers. If your sales drop for two straight months, your forecast adjusts. Your budget does not.

3) Flexibility: A budget stays fixed once approved. A forecast keeps changing. If your coffee shop is earning less than expected, your forecast will reflect that immediately, so you can react.

4) Usage: You use a budget to plan. You use a forecast to manage. One sets direction. The other helps you stay on track.

When you’re building your financials, you don’t have to start from scratch. You can begin with a simple budget and forecast template to structure your numbers and assumptions.

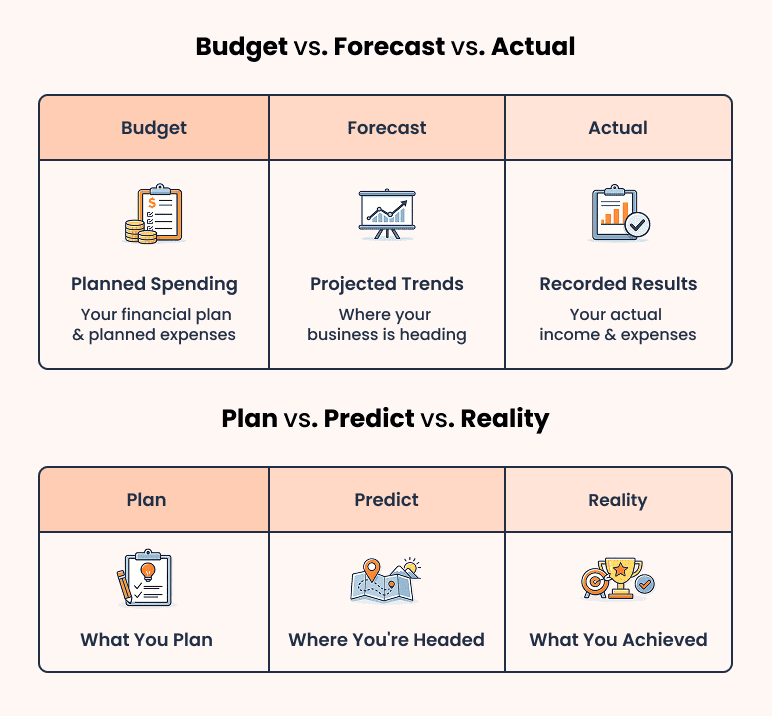

Budget vs. forecast vs. actual: How all three work together

We’ve already discussed the forecast vs budget. Let’s define one missing piece, “actuals”.

The "actuals" mean your real, recorded financial results. Not what you planned, not what you predicted, but what actually hit your bank account and expense ledger.

The relationship works like this:

- You start the year with a budget (your plan)

- Update your forecast throughout the year as new data comes in (your prediction)

- Compare both against your actuals (your reality) at the end of each period

This comparison is called variance analysis, and it's simpler than it sounds. You're just asking, how far off were we, and why?

Here’s the coffee shop example. The owner budgets $10,000 in monthly sales. By the end of Q1, foot traffic is softer than expected, so the forecast gets revised down to $8,500. April closes, and actual sales come in at $9,200.

That's a positive variance against the forecast, and only a modest miss against the budget.

| Metric | Amount ($) |

|---|---|

| Budget | $10,000 |

| Forecast | $8,500 |

| Actual | $9,200 |

Now comes the important part: variance analysis.

Variance simply means the difference between these numbers.

- Actual vs Budget → You missed your target by $800

- Actual vs Forecast → You performed $700 better than expected

This is where real insights come from. You can ask: Did sales drop due to fewer customers? Or did pricing change? Was the forecast too conservative?

Once you identify the reason, the next step is action. If customer traffic dropped, you might invest in local marketing or run promotions to bring people in.

If pricing is the issue, you could adjust your menu prices, offer bundles, or test discounts. If your forecast was too conservative, you may revise future projections and increase inventory or staffing to meet demand.

The goal is simple. Use variance not just to understand what happened but to decide what to do next.

Instead of guessing, you now have clear signals.

This three-way comparison helps you stay grounded. Your budget keeps you focused. Your forecast keeps you realistic. Your actuals keep you honest.

When to use a budget, a forecast, or both

The answer depends on where your business is right now.

Different stages of business need different financial tools and financial techniques. Using the wrong one or skipping both can lead to poor decisions. Here’s how to think about it.

| Scenario | What to Use | Why It Matters |

|---|---|---|

| Pre-launch startup | Bottom-up forecasting | No historical data. Build estimates from services, pricing, and expected jobs to test viability |

| Established business (2+ years) | Budget + Forecast | Budget sets targets. Forecast adjusts based on real performance and trends |

| Seeking funding / business plan | Top-down + Bottom-up forecasting + Budget | Top-down shows market potential, bottom-up shows realistic numbers, budget shows control |

| Rapid-change environment | Rolling forecast + Flexible budget | Updates numbers regularly based on actuals and helps adjust decisions quickly |

Now, let’s break down why this matters in practice.

If you’re a pre-launch startup, you don’t have past numbers to rely on. Any budget you create is mostly guesswork. A forecast helps you test assumptions like pricing, demand, and costs before you commit to fixed targets.

For established businesses, both tools become important. Your budget gives structure and keeps spending in control. Your forecast helps you adjust when actual performance shifts. This balance helps you stay disciplined while still being responsive.

When you’re seeking funding or writing a business plan, both are expected. Lenders want to see that you have a clear spending plan and realistic projections. One shows intent. The other shows expected outcomes.

In fast-changing environments, relying only on a fixed budget can slow you down. A rolling forecast allows you to update numbers regularly and react quickly. Pairing it with a flexible budget helps you adjust spending without losing control.

If you can only choose one, start with a forecast. It gives you a clearer picture of what’s likely to happen.

Writing a business plan? Remember, you need both. Your financial projections section is essentially a forecast. Tools like Bizplanr can help you generate both quickly and then refine them based on your assumptions.

Common budgeting and forecasting mistakes to avoid

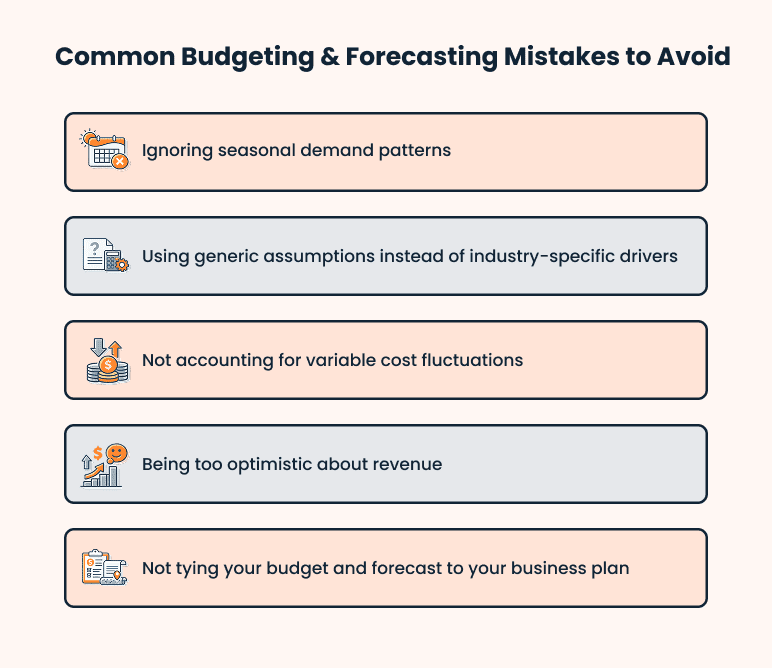

Most budgets fail not because the numbers are wrong, but because they never get updated.

Here are the most common mistakes that quietly hurt your financial planning:

The first is failure to consider the seasonal demand patterns. There are seasonal highs and lows in many businesses, and this is particularly true in retail, hospitality, and services. Unless these cycles are reflected in your budget, your projections will appear solid and work. This usually results in overstocking during slack months or missing chances in high seasons.

Next, it is to use generic assumptions, rather than industry-specific drivers. Every business operates on various measures. A SaaS company has to keep track of subscriptions and churn, whereas a restaurant relies on foot traffic and table turnover. When these drivers are not included in your budget and forecast, your numbers will not be what they are.

Then there is the third error, which is the failure to consider the variation of the cost of variables. Costs, which include raw materials, fuel, or prices of suppliers, can fluctuate fast in an industry such as manufacturing, logistics, or food. Assuming that your forecast is of constant costs may cause pressure on the margin and cash flow problems in the event of price changes.

In addition, overly optimistic about revenue. Many founders rely on business plan assumptions of greater sales than they would receive. This causes impractical expectations and, in most cases, extravagance that strains cash flow in the future.

The last mistake is not linking your budget and forecast to your business plan. Your financial numbers should support your strategy. If they don’t connect with your goals, hiring plans, or growth direction, they become disconnected from how your business actually runs.

These gaps often show up clearly when you write your business plan conclusion, where everything should come together. If your numbers and strategy don’t connect there, it’s a sign that something needs to be fixed.

How to add a budget and forecast to your business plan

The good news? You don’t have to build your budget and forecast from scratch. A business plan combines both budget targets and forecast estimates into one financial projection section.

When you’re writing a business plan, your financial projections section is essentially your forecast. It shows expected revenue, expenses, and cash flow over time. This is what lenders and investors focus on to understand if your business is viable. Even the SBA recommends including financial projections in every business plan to show how the business will perform.

Alongside this, your budget acts as your internal plan. It outlines how you intend to manage spending and hit your targets. While projections show where you’re heading, your budget shows how you plan to get there.

Most lenders expect to see both. They want to know your targets and your expected outcomes based on realistic assumptions.

To build these faster, tools like a financial model generator can help. Instead of starting from a blank sheet, you input basic details like revenue streams, costs, and growth assumptions. The tool then creates structured projections that you can refine.

This approach saves time and reduces errors, especially if you’re not from a finance background.

Limitations to understand:

Budgets can create a false sense of control if you don’t update them regularly. Forecasts can go wrong if you use unrealistic assumptions or outdated data. Relying on only one without the other creates blind spots in decision-making.

A business plan, budget, and forecast work together as one system. The business plan sets your strategy, the budget defines how you will spend and allocate resources, and the forecast tracks actual performance over time. Using all three together helps you plan clearly and adjust decisions as your business grows.

Use Bizplanr's AI to generate a first draft of financial projections in minutes. Then customize based on your own research and assumptions.

Conclusion

You now understand how budgeting and forecasting work together in business planning. A budget sets your targets, a forecast shows your expected direction, and comparing both with actual results helps you make better decisions over time.

Your budget shows how you plan to allocate resources, while your financial projections section reflects your forecast.

In simple terms, a budget defines your targets, a forecast tracks real performance, and comparing both with actual results helps you identify gaps and adjust decisions.

Including both in your business plan shows clear goals and realistic expectations to lenders and investors.

To make this easier, you can use a financial model generator to quickly create structured projections. Then refine them based on your assumptions and research.

You can also explore how to build accurate financial projections in your business plan to strengthen your plan further.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

What is the difference between the actual budget and the forecast?

A budget sets your planned revenue and expenses. A forecast predicts likely results based on current data and trends. Actuals are your real financial results. Comparing all three helps you see if you met your targets and where you went off track.

What comes first, budgeting or forecasting?

In most cases, budgeting comes first. You set targets through a budget, then use a forecast to track if you'll meet them. However, startups without past data may begin with a forecast.

What is the difference between a budget and a financial projection?

A budget is an internal spending plan. A financial projection is a forecast that estimates future revenue, expenses, and cash flow. In a business plan, financial projections are essentially your forecast.

Can you run a business without a budget?

Some early-stage startups operate with only a forecast. But a budget helps control spending and measure performance. Most lenders expect both before approving funding.

How often should you update a forecast?

At a minimum, update your forecast quarterly. Monthly updates are better, especially if your business changes quickly. Many businesses now use rolling forecasts to stay current.

Follow Vinay Kevadiya