Most entrepreneurs I talk to can put together an income statement without too much trouble. The balance sheet forecast is the one that stops them cold.

Though you may have tried building one, halfway through, the questions start piling up: What goes where? How do I project accounts receivable if I haven't made a sale yet? Why won't this thing balance? And how does it even connect to my income statement or cash flow?

That confusion is a problem because lenders and investors go straight to the balance sheet to check your debt load, working capital, and equity position before they engage with anything else in your plan.

So let me show you exactly how to forecast a balance sheet for building financial projections for your business plan.

What is a balance sheet forecast?

A balance sheet shows where your business stands right now, and a balance sheet forecast shows where it's headed.

More specifically, it's a projection of three things at a future point in time:

- Assets: What your business owns (cash, accounts receivable, inventory, equipment)

- Liabilities: What your business owes (accounts payable, loans, credit lines)

- Equity: What's left after you subtract liabilities from assets

Every balance sheet runs on one equation:

Assets = Liabilities + Equity

That equation has to hold in every period you forecast and not just the final year. If it doesn't, it’s a sign that something's off somewhere in your model.

The regular balance sheet uses numbers from your books, while a forecast uses your revenue projections, expense assumptions, and business plans to estimate what those numbers will look like down the road.

Why your business might need a balance sheet forecast?

If you're still in early planning mode, you might not need this yet. But the moment you walk into a bank, pitch an investor, or decide to hire your first employee, the balance sheet forecast becomes part of the conversation.

Most founders I work with are laser-focused on revenue and profit, and that makes sense. But lenders and investors don't stop there. They want to see what the business actually owns, what it owes, and whether the numbers hold together beyond the income statement. Here's where it becomes relevant:

SBA loan applications

SBA lenders require a full set of projected financial statements, and the balance sheet is part of that package. In fact, SBA loan application requirements specify that 3-year projected financial statements are mandatory for most loan applications.

A well-built forecast shows that you understand your debt obligations and have a realistic picture of your financial position over the next three years.

Investor evaluation

Investors check your balance sheet before they engage with your growth story. They want to see your debt levels, working capital, and equity position to get a sense of how much risk they're taking on.

Cash planning

Your balance sheet forecast shows where money might get tied up before it reaches your bank account. If your receivables grow from $20K to $50K as revenue scales, that's $30K sitting in unpaid invoices. You've earned it, but you can't spend it yet. Knowing that in advance is what keeps a cash crunch from turning into a crisis.

Hiring and expansion

Before you commit to a new hire or a second location, your balance sheet forecast tells you whether the business can actually support it. It shows whether your assets are growing in line with your plans and whether you have the capacity to take on additional costs without stretching your finances too thin.

Debt financing

When you apply for a line of credit, banks, apart from looking at your revenue, calculate ratios like debt-to-equity and current ratio directly from your balance sheet. A forecast that shows healthy ratios over time gives lenders confidence that you can service the debt without putting the business at risk.

Build your balance sheet forecast in 12-month increments and summarize annually. That's the format SBA lenders will ask for.

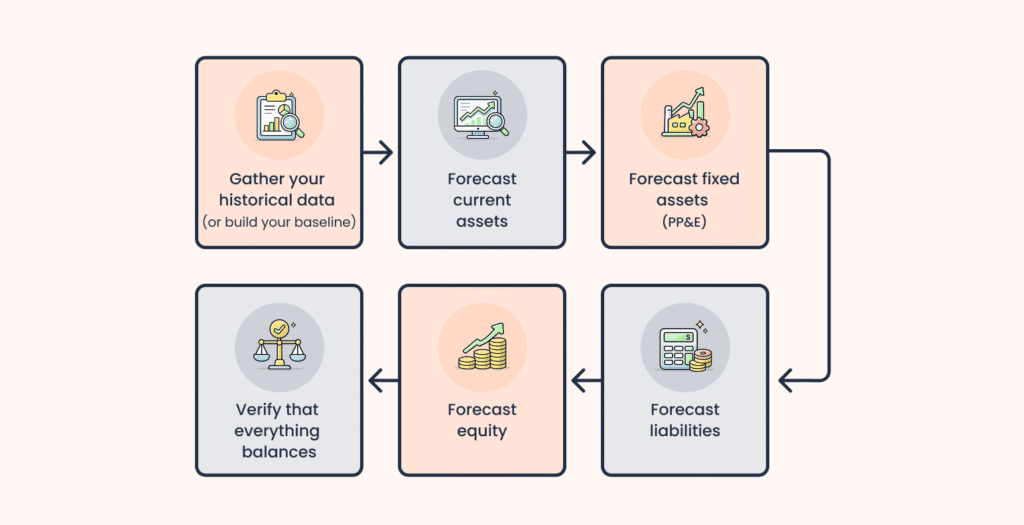

How to forecast a balance sheet: Step-by-step

Over time, I’ve found that breaking the balance sheet into a few clear steps makes it much easier to build. Here’s how I approach it.

Step 1: Gather your historical data (or build your baseline)

If you're an existing business, pull your most recent balance sheet directly from your accounting software, QuickBooks, Xero, or whatever you use. I'd recommend looking at the last one to two years if you can. Patterns in receivables, payables, and inventory tell you a lot about how your business actually operates, and those patterns will inform your assumptions going forward.

If you're a new business with no financial history, your baseline comes from your income statement projections. Start by projecting your revenue, cost of goods sold, and operating expenses.

From there, build your opening position:

- Cash from owner investment or loans.

- Any initial assets, like equipment or setup costs.

- Any starting liabilities, like loans or credit balances.

This becomes your Day 1 balance sheet.

The key idea is that you have to anchor your forecast in either actual financials or assumptions you've already made elsewhere in your plan. In my experience, when this step feels unclear, it's usually a sign that the revenue and expense projections need more work first. Everything downstream depends on them.

Traditionally, this whole process meant hours in a spreadsheet, building formulas, linking statements manually, and debugging when things didn't balance. I know founders don't have that kind of time, and honestly, they shouldn't need to.

You can also use any generative AI tools to pressure-test your revenue assumptions or think through your cost structure before you start. That works too. The point is, the manual version of this process is optional now.

Step 2: Forecast current assets

The current assets are the short-term items that keep your business running day to day. These don't come from fixed numbers. They come from how your business collects cash, manages stock, and handles timing.

I find it helpful to ask one question here: where is my money sitting before it becomes cash? The answer is your net working capital, the difference between your current assets and current liabilities, and it's one of the first things lenders check.

To answer that, break current assets into three core components:

Accounts Receivable (AR)

This is revenue you’ve already earned but haven’t collected yet. So if you’re wondering how to estimate this, simply base it on how long customers take to pay.

AR = (Days Sales Outstanding (DSO)) ÷ 365 × Revenue

DSO = average number of days customers take to pay

Revenue: $500,000 | DSO: 30 days

AR = (30 ÷ 365) × $500,000 = $41,096

That's roughly $41K sitting in unpaid invoices at any given time. You've earned it, it just hasn't landed in your account yet.

Inventory

This is the value of goods sitting before they’re sold. If you don’t have clear inventory data, estimate it based on how long the inventory stays unsold.

Inventory = (DIO ÷ 365) × COGS DIO (Days Inventory Outstanding) = how long stock sits before selling

If inventory sits for 45 days and your COGS is $200,000, the inventory value should be around $24,657.

However, if you run a service-based business, this line may not apply.

Cash

Cash is the actual money available in your business at any point in time, your bank balance, petty cash, and any short-term liquid holdings.

Unlike AR and inventory, you don't calculate cash directly on the balance sheet. It gets pulled from the closing balance on your cash flow statement. Your operations determine profit, your cash flow statement adjusts that into actual cash movement, and the balance sheet simply reports what's left.

If your cash number doesn't match your cash flow statement, immediately go back and check your earlier assumptions.

There's a faster way. Put your assumptions into Bizplanr, and your entire financial model builds itself, balance sheet included. Lender-ready in minutes. [Get started →]

Step 3: Forecast fixed assets (PP&E)

These are long-term assets your business uses over time: equipment, machinery, vehicles, computers, and similar physical resources.

Most small business forecasts don't need a detailed asset schedule. However, you need to capture two important things:

- What you're planning to buy

- How those assets lose value over time

PP&E = Prior Year PP&E + CapEx − Depreciation

CapEx (Capital expenditure)

This is where you account for new purchases: equipment upgrades, machinery, vehicles, and tools. If you know your growth plans, plug those numbers in directly. If you don't, a common approach is to estimate CapEx as 3-5% of revenue to keep the model grounded without overcomplicating it.

Depreciation

Depreciation reduces the book value of your assets each year. I'd recommend keeping this simple: use straight-line depreciation and spread the cost over the asset's useful life.

Say you start the year with $50,000 in equipment. You buy $10,000 worth of new machinery, and depreciation for the year comes to $5,000. Your ending PP&E is $55,000.

PP&E doesn't shift every month unless you're actively buying something. In most early-stage models, it stays relatively stable, with small depreciation adjustments each period.

If you run a service business, this section will be simple. If your business depends heavily on equipment or physical infrastructure, give it more attention. It has a direct impact on your asset base and how depreciation flows through your financials over time.

Step 4: Forecast liabilities

Most early-stage balance sheets come down to two main items:

Accounts payable (AP)

AP is money you owe to suppliers or vendors but haven't paid yet. Just like receivables, it's based on timing: how long you typically take to pay.

AP = (Days Payable Outstanding (DPO) ÷ 365) × COGS DPO = average number of days you take to pay suppliers

If you pay suppliers in 40 days and your COGS is $200,000, your AP sits around $21,918. That means at any point, roughly $22K is owed but not yet paid.

If you don't have past data, use your expected payment terms: 15, 30, or 45 days are all reasonable starting points.

Long-term debt

This covers loans, credit lines, and any structured borrowing. You don't just carry the loan amount forward. You need to account for both new borrowing and repayments.

Debt = Previous Balance + New Borrowings − Principal Repayments

Say you start with a $100,000 loan, take on a new $50,000 loan, and make $20,000 in principal repayments during the year. Your ending debt balance is $130,000.

Always remember that only principal repayments reduce the loan balance, and interest payments belong on your income statement, not here.

If you're planning new funding like an SBA loan, add it as a separate line. It keeps your capital structure transparent and makes it easier for lenders to follow.

One thing I always check at this stage is whether liabilities are growing in line with the business. If your COGS increases, your payables should increase with it. If they don't, something is not right in your assumptions.

Step 5: Forecast equity

Equity is what's left for the owner after every liability is accounted for. It's not a static number and moves every period based on how the business performs and what you do with the profits.

In my experience, this is the section founders pay the least attention to, and it's usually because they're not sure where profit actually ends up. It doesn't stay on the income statement. It flows into equity.

At a basic level, equity changes in two ways:

- through profits or losses the business generates

- through the money you put in or take out

Retained Earnings

This is where your profits accumulate over time. Every dollar of net income that isn't withdrawn stays here and builds period over period.

Closing Retained Earnings = Opening RE + Net Income − Dividends

Net income flows in from your income statement. Withdrawals or dividends reduce the balance.

Let’s say you start the year with $10,000 in retained earnings, generate $80,000 in net income, and withdraw $20,000. Your closing retained earnings are $70,000. And next year, that $70,000 is your new opening balance. It doesn't reset.

Owner's Capital/Paid-in Capital

This reflects money invested directly into the business, either your own funds or outside investment. It only changes when new capital comes in.

If you invested $50,000 to start and added $25,000 later, your paid-in capital is $75,000. One thing I want to flag here: this has nothing to do with profit. Adding capital increases equity, but it doesn't touch your income statement.

Once this section is filled in, read equity as a signal. A growing equity balance usually means the business is profitable and retained earnings are building. A shrinking balance means losses are eating into ownership value. If those signals don't show up in your model, something upstream isn't connected properly.

Step 6: Verify that it balances

Once you've filled in all sections, run this check:

Total Assets = Total Liabilities + Total Equity

If this holds, your model is internally consistent. If it doesn't, something is missing or not connected properly. Don't try to fix it by adjusting numbers randomly. The balance sheet should balance naturally when everything is linked correctly.

The issue almost always comes down to one of three things:

- Cash not linked properly: Your cash balance must come directly from your cash flow statement. If you've entered it manually, it will likely break the model.

- Working capital changes not captured: Changes in AR, inventory, or AP must be reflected in your cash flow statement. If they're not, the statements fall out of sync.

- Debt or equity updates missing: New loans, repayments, or capital injections must appear consistently across all three statements.

The way I debug this is to go line by line and ask: if this number changed, where does that change show up in the cash flow? Every movement on the balance sheet has a cash impact somewhere. If you can't trace it, that's the problem.

Also, don't wait until the final year to run this check. Verify the equation for every forecast period. Small gaps in Year 1 tend to compound through Years 2 and 3, and by then they're much harder to untangle.

Key balance sheet forecasting formulas (Quick reference)

If you strip everything down, balance sheet forecasting comes back to a handful of repeatable formulas. I usually keep these in one place because you’ll end up using them every time you build or review a model.

| Line Item | Formula | Method |

|---|---|---|

| Accounts Receivable | (DSO ÷ 365) × Revenue | DSO (collection timing) |

| Inventory | (DIO ÷ 365) × COGS | DIO (inventory timing) |

| PP&E | Prior PP&E + CapEx − Depreciation | Asset schedule |

| Accounts Payable | (DPO ÷ 365) × COGS | DPO (payment timing) |

| Long-Term Debt | Prior Debt + New Borrowings − Repayments | Debt schedule |

| Retained Earnings | Prior RE + Net Income − Dividends | Income statement link |

If you're an existing business, pull your DSO, DIO, and DPO from the last two to three years of financials. If you're new, start with industry benchmarks and refine as actual data comes in.

Cross-check your DSO, DIO, and DPO assumptions against NAICS industry averages before presenting to lenders or investors. Assumptions that fall way outside industry norms will raise questions you don't want to answer mid-pitch.

How to forecast a balance sheet with no historical data?

If you're just starting with no financial history, you have to build the balance sheet forecast from assumptions that are grounded in something real.

I'd start with the income statement projections. Your revenue, COGS, and operating expenses are what drive most of your balance sheet line items. Receivables follow from revenue, and inventory and payables follow from COGS.

For timing ratios like DSO, DIO, and DPO, I'd borrow from NAICS industry benchmarks rather than making them up. Standard payment terms like net 30 or net 45 also work as a starting point.

A few things I'd keep in mind:

- Build a Day 1 opening position: the cash you're putting in, any equipment you're buying, and loans you're taking on.

- Keep Year 1 conservative as early operations are almost always less efficient than you expect.

- Use industry benchmarks in Year 1 and adjust in Years 2 and 3 as real data comes in.

- Once you're 6 to 12 months in, replace assumptions with actual numbers.

Build multiple scenarios (Don't just forecast once)

A lender would want to know if you can still service your debt if revenue comes in 15% lower than expected, whereas an investor would look at what the upside looks like if it comes in 20% higher. Naturally, the same forecast can't answer both, so presenting only one number to either of them doesn’t make sense.

I always run three: a conservative case, a base case, and an upside case. The conservative one is where lenders spend most of their time, upside is what gets investors leaning forward, and the base case is what you actually believe.

What I find most useful about running all three is watching how the balance sheet responds.

- Do assets grow in line with revenue?

- Does debt increase to support expansion?

- Does equity hold up?

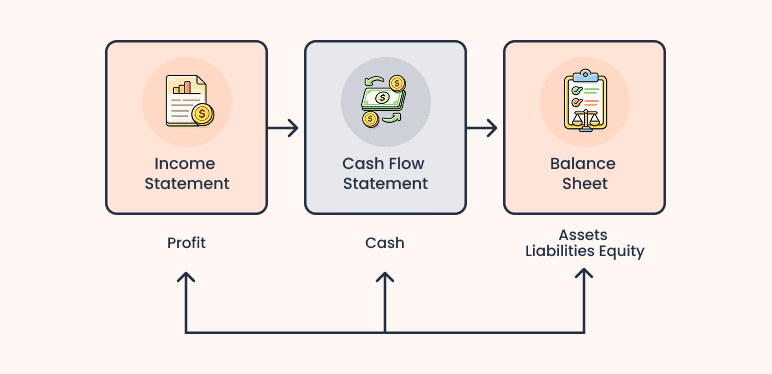

Where does a balance sheet forecast fit in your business plan?

The balance sheet forecast sits in the financial section of your business plan, alongside the income statement and cash flow statement.

It's not something you build first. It comes at the end.

Your financials follow a sequence:

- The income statement shows revenue, expenses, and profit.

- The cash flow statement adjusts that into actual cash movement.

- The balance sheet forecast shows your financial position at a specific point in time.

That order is important because the balance sheet forecast depends on both. Net income flows in from the income statement. Cash comes from the cash flow statement. Everything else connects from there: receivables, inventory, payables, debt.

One way to think about it: when revenue grows, receivables usually grow with it. When you take on a loan, both cash and liabilities increase. These relationships are what make the model consistent.

This is also where things get validated. If something doesn't line up on the balance sheet, it usually means something earlier in the model needs fixing.

That's why the balance sheet is built last. Together, these three statements form what's called a 3-statement financial model, and it's the standard format lenders and investors expect to see in a business plan.

If you're raising a loan through the SBA, the funding requirements section of your business plan should reference your balance sheet forecast directly—specifically, your projected debt load and equity position.

Build your financial forecasts with Bizplanr

Though you might think the real challenge is building a balance sheet forecast once, I’d argue it’s keeping everything connected as and when the numbers change.

That’s where Bizplanr can really make a difference in your financial forecast. Instead of rebuilding each statement every time something changes, you update your assumptions once, and all three statements adjust together.

The same logic applies across the model. If you add funding, debt and cash update automatically. Bizplanr keeps everything consistent without you having to track every link manually. When you run different scenarios, there’s no need to rebuild anything. You adjust inputs once, and your financial position updates across all three statements.

Once you’re done, your financials export directly into your business plan, structured and ready to share.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

What is the difference between a balance sheet and a balance sheet forecast?

A balance sheet is an overview of what your business owns and owes right now, pulled from your actual financial records. A balance sheet forecast projects what that snapshot will look like at a future date, based on your revenue, expense, and operational assumptions.

How do you forecast accounts receivable on a balance sheet?

You base it on how long customers typically take to pay, using the DSO method. The formula is: AR = (DSO ÷ 365) × Projected Revenue. If your DSO is 30 days and you're projecting $500,000 in revenue, your AR balance sits around $41,096.

Can you forecast a balance sheet without a cash flow statement?

Technically, yes, but it's not recommended. Your cash balance on the balance sheet should come directly from the closing balance on your cash flow statement. Without that link, your cash figure is a rough estimate at best. The right sequence is income statement first, cash flow second, balance sheet last.

How far ahead should I forecast my balance sheet?

Most lenders and investors want to see three years of projected financial statements. I'd recommend forecasting monthly for Year 1, where cash flow visibility matters most, then annually for Years 2 and 3. SBA loan programs specifically require three-year projections, so building to that standard from the start saves you the work later.

Follow Kaylee Philbrick-Theuerkauf