According to CB Insights, 29% of startups fail simply because they ran out of cash. The last thing you want is to be in that group because you handed a lender a forecast you weren't fully confident in.

There's no shortage of guides on creating a cash flow forecast, but the problem is — most are either too vague, too technical, or written for a completely different audience.

This one breaks it down into 5 clear steps, with real numbers and a US-based example. Hopefully, you won't need to read another guide on this after today.

What is a cash flow forecast?

A cash flow forecast shows you how much cash you'll have in your business at any given point in the future. I think of it as a window into the next few weeks or months. It tracks when money is actually expected to land in your account and when it's going out, so you can see what your balance looks like before it happens.

It's a planning tool. You build it to answer questions like:

Can I cover payroll next month? Will I have enough left after Q1 expenses to hire a contractor?

You might wonder how a cash flow statement fits into this, since it looks almost identical.

Cash flow forecast vs. Cash flow statement

The statement is a historical record of how cash moved through your business in the past, mostly used for accounting, tax reporting, and financial reviews. The forecast is about what's ahead.

Founders and operators use the forecast regularly, updating it weekly or monthly as new information comes in. The statement is prepared periodically by accountants for reporting and tax purposes. They share the same structure, but serve completely different purposes.

Now that you know what a cash flow forecast is, let's talk about what actually goes into it.

What goes into a cash flow forecast?

A cash flow forecast is built on three things: what you're starting with, what's coming in, and what's going out. That's it.

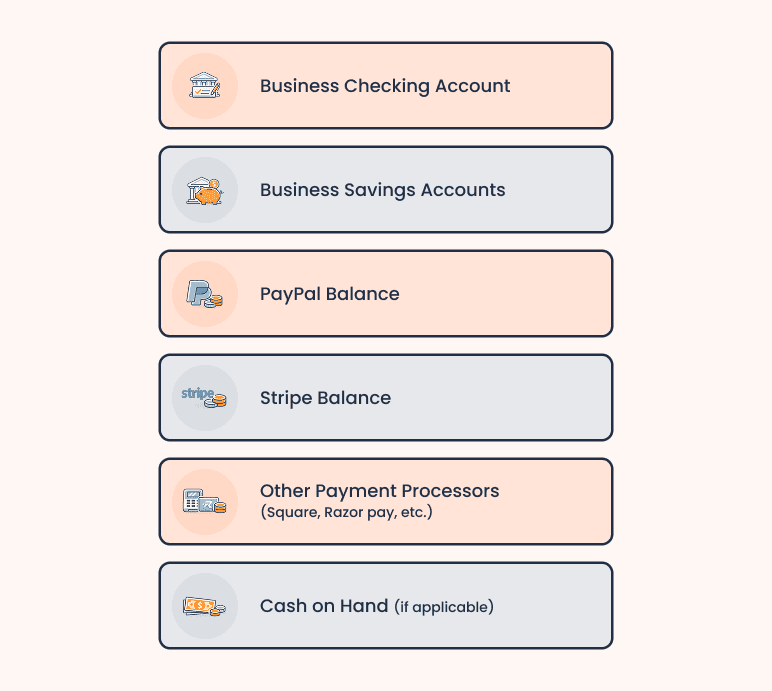

1. Opening cash balance

This is the actual cash sitting in your accounts at the start of the forecast period. Checking, savings, PayPal, Stripe, or anything where your business holds or receives money. It doesn't include accounts receivable, inventory, or anything you're expecting but haven't received yet.

2. Cash inflows

This is every dollar you expect to receive during the forecast period. For most small businesses, that includes

- Customer payments

- Loan disbursements

- Grants

- Tax refunds

- Asset sales

The important thing to keep in mind is timing. Log each inflow for the period when the cash actually lands in your account, not when you invoice or earn it.

3. Cash outflows

This is every dollar leaving your business during the period. That covers payroll, rent, utilities, insurance, supplier payments, loan repayments, subscriptions, owner draws, and IRS estimated tax payments due April 15, June 15, September 15, and January 15. Include everything, even expenses that only come up a few times a year.

Once you have all three, the math is quite simple:

Closing balance = Opening balance + Inflows − Outflows

That closing balance rolls forward as the next period's opening balance. If any period shows a negative number, that's your early warning signal. You now have time to adjust before it becomes a real problem.

Before we get into how to create one, let's quickly walk through the two ways it can be done. It'll make the steps easier to follow.

Before you start, choose the right forecasting method

The direct method tracks actual transactions, customer payments, bills, payroll, and rent. It gives you a clear, granular picture of cash moving in and out, which is why I'd recommend it for most small business owners, especially if you're managing cash closely week to week.

The indirect method starts with net income and adjusts for non-cash items like depreciation, changes in receivables, and inventory movement. It's more commonly used for investor reporting or long-term planning across multiple business units.

| If you… | Use this method |

|---|---|

| Have fewer than 100 transactions/month | Direct |

| Use QuickBooks, Xero, or accrual software | Indirect |

| Are preparing a business plan or SBA application | Indirect |

| Want granular daily cash visibility | Direct |

| Are presenting to investors or lenders | Indirect |

| Run a cash-heavy business and need both views | Both |

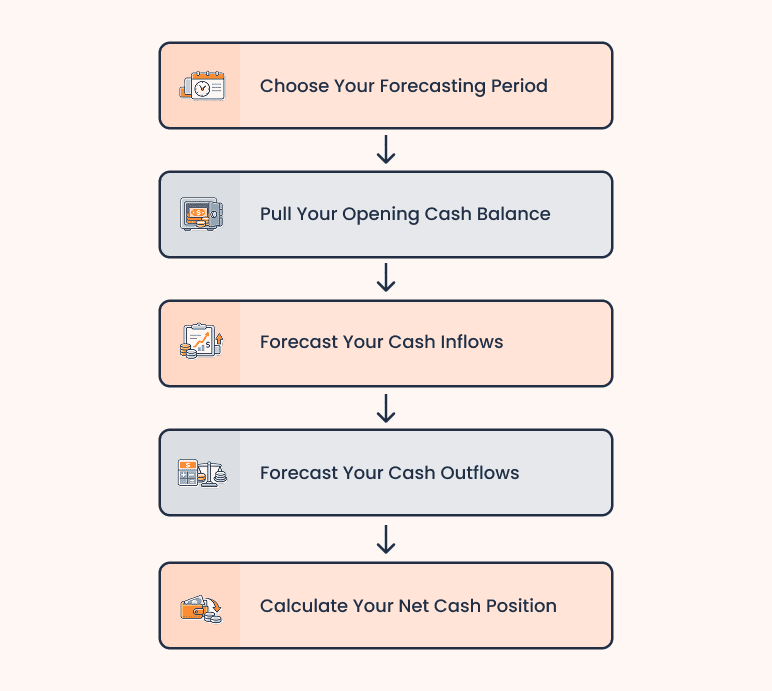

How to create a cash flow forecast (5 easy steps)

Building a cash flow forecast comes down to five steps. Here's the process I'd walk any first-time business owner through:

Let's go through each one.

Step 1: Choose your forecasting period

Decide how far out you're forecasting and at what level of detail. For most small businesses, a 12-month forecast is the right starting point. It gives enough visibility to plan without overcomplicating things.

The correct timing is based on the reason why you want to make the prediction in the first place. Here's how to think about it:

- 13-week (weekly): This is for when you need close visibility on cash week by week. It's the standard for cash-tight situations, pre-revenue startups, and short-term financing applications. Many lenders and bankruptcy trustees require it specifically because it shows exactly where the pressure points are.

- 12-month (monthly): This is the standard for most small business planning. Banks and SBA lenders typically require a 12-month forecast as part of a loan application, and it's the right format for business plan writing, annual budgeting, and general financial planning.

- 3-5 years (quarterly/annual): This is used mostly for investor presentations and long-term strategic planning. If you're writing a 3-year business plan, a quarterly forecast gives you the direction you need without false precision. The further out you go, the less accurate it gets, but it's useful for evaluating major decisions and setting direction.

If you're applying for an SBA loan, build a 12-month monthly forecast and a 13-week weekly forecast. The 12-month forecast will be for the lender, and a 13-week weekly forecast will manage your cash during the application process, which can take anywhere from 60 to 90 days.

Step 2: Pull your opening cash balance

Log into every account your business uses and note the current balance. Write down the actual number you see today.

This is your starting point, and it needs to be exact.

A question I get here: What about business credit cards or lines of credit? Don't include them as cash. They're liabilities. If you draw on a line of credit during the forecast period, that shows up as a cash inflow at the point you actually receive the funds.

Step 3: Forecast your cash inflows

List every source of cash you expect to receive during the period and, more importantly, when it will actually arrive. If a client owes you $20,000 on net-30 terms, that's not January cash. It's February cash. Shift every invoice forward based on your actual payment terms.

A simple rule I use when I'm unsure whether to include a payment: would I rely on this money to pay my bills? If the answer is no, either delay it or leave it out.

A few things to keep in mind when forecasting inflows:

- Don't assume perfect behavior. If a client usually pays late, reflect that. A net-30 invoice that typically gets paid in 45 days belongs in the later period, not where it's supposed to land.

- Be realistic about your pipeline. Not every deal will close on time. If you're expecting $10,000 in new business but only 70% is likely to come through, forecast $7,000.

- Forecast each payment individually. Cash doesn’t come in evenly. If two payments of $5,000 land in March and one in April, show $10,000 in March and $5,000 in April, not $7,500 in both.

If you're just starting out with no clients yet, base your inflows on signed contracts and conservative estimates. Working through your business plan assumptions first will give you more grounded numbers to work from. When in doubt, use the lower number.

Step 4: Forecast your cash outflows

List every dollar you expect to pay out during the period. I'd recommend going through your last three bank statements rather than relying on memory. You'll almost always find something you forgot.

Group your outflows by category:

- Payroll and contractor payments

- Rent and utilities

- Insurance

- Supplies and inventory

- Loan repayments

- Subscriptions and software

- Owner draws

- IRS estimated tax payments (Apr 15, Jun 15, Sep 15, Jan 15)

A question I get often is whether to include the owner's salary or personal draws. Yes, always. If money is leaving the business account, it belongs in the forecast regardless of where it's going.

The expenses that catch people off guard are the irregular ones. A quarterly tax payment or an annual insurance renewal can completely change the picture for that month. If it's a real expense, it belongs in the forecast.

Step 5: Calculate your net cash position

For each period, apply this formula:

Closing balance = Opening balance + Inflows − Outflows

That closing balance becomes the opening balance for the next period. Repeat this across every week or month in your forecast.

This is where the forecast becomes your decision tool. You can now track whether your cash is building or shrinking over time, and that pattern tells you a lot about the health of your business.

A positive closing balance means you have enough cash after covering expenses. A declining balance, even if still positive, is worth paying attention to. It means you're heading toward a shortfall before it actually shows up.

If any period shows a negative number, I'd actually call that a win because you found it early enough to do something about it. At that point, you have real options:

- Delay a planned expense

- Speed up collections

- Adjust payment terms

- Arrange short-term financing before the gap arrives.

To keep a current forecast, you should set a reminder to refresh your forecast at the end of each month. Compare projected to actual, revise the following 3 months, based on new information, and roll the forecast forward.

How do you forecast cash flow for a seasonal business?

If you have a seasonal business, I'd say timing becomes the most critical part of the forecast. Rather than distributing the revenue evenly on a monthly basis, graph your year as high, moderate, and low. The money you receive in the active months is what sustains you during the slow months, and your forecast must account for both the peaks and the valleys.

Your strongest month doesn't help if you haven't planned for what the slowest months will cost you. Use your peak month projections to set a cash reserve target, so when the slow months hit, you're drawing from a cushion you already planned for.

Cash flow forecast example (with real numbers)

Here's what a three-month cash flow forecast looks like for a real US small business, including a month where the net cash goes negative.

Let's use Peak Advisory, a two-person marketing consulting firm in Austin, Texas, as our example. Here's what their first quarter looks like:

| Line items | January | February | March |

|---|---|---|---|

| Opening Balance | $12,000 | $18,700 | $20,200 |

| Inflows | |||

| Client Payments | $28,000 | $22,000 | $18,000 |

| Total Inflows | $28,000 | $22,000 | $18,000 |

| Outflows | |||

| Contractor Payments | $14,000 | $14,000 | $14,000 |

| Rent | $2,500 | $2,500 | $2,500 |

| Software Subscriptions | $800 | $800 | $800 |

| Q4 Tax Payment | $4,000 | — | — |

| Credit Card Payment | — | $3,200 | — |

| New Equipment | — | — | $8,000 |

| Total Outflows | $21,300 | $20,500 | $25,300 |

| Net Cash | +$6,700 | +$1,500 | -$7,300 |

| Closing Balance | $18,700 | $20,200 | $12,900 |

January is a strong month. Client payments come in at $28,000, and even with the Q4 tax payment hitting, Peak Advisory closes with $18,700. In February, one client delayed payment, bringing inflows down to $22,000. Outflows come in at $20,500, which leaves a net cash of $1,500 and a closing balance of $20,200. The balance grew, but outflows consumed nearly all of the month's inflow.

March is where the forecast proves its value. Monthly inflows drop to $18,000, and a planned purchase of equipment amounting to 8,000 moves total outflows to 25,300. The outcome is a negative cash flow of $7,300 and a final balance of $12,900.

That was a negative figure in March, and it is an indicator, not a crisis. Peak Advisory now has two months to respond. They could delay the equipment purchase to Q2, push clients to settle outstanding invoices earlier in February, or arrange a small line of credit to cover the gap. Any one of those moves changes the March picture entirely.

That's exactly what a forecast is for.

Conclusion

Now you have all you need to create a cash flow forecast that does not fall apart. The steps are not complex; the only difference between a working forecast and one that sits in a folder is the discipline of updating it monthly.

Remember, at the very end of every month, sit down with your actuals and make amendments. You will quickly find that you begin to notice trends in your own business that you never noticed before.

And when you are filing this with a loan or a business plan, you have to remember that a cash flow forecast is only part of the picture. Your lenders will also be interested in viewing your larger financial projections. Bizplanr's financial planning tools handle both, so you're not figuring out lender requirements on your own.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

What is a cash flow forecast?

A cash flow forecast tells you how much money will be in your business at any given time in the future, depending on what you are likely to receive and spend. It is not the paper money on profit or revenue. It is in real cash, in your account, on a particular date. More importantly, so you can spot shortfalls before they become emergencies.

What is the difference between a cash flow forecast and a cash flow statement?

A cash flow statement is a historical record of how cash moved through your business. A forecast looks forward, helping you make decisions before cash problems appear rather than reporting on them after the fact.

How far ahead should you forecast cash flow?

Most small businesses should start with a 12-month rolling cash flow forecast reviewed monthly. If cash is tight or you're applying for short-term financing, a 13-week weekly forecast gives you better visibility. The further out you project, the less precise it gets, but knowing you might fall short six months ahead gives you far more options than finding out two weeks before it happens.

How do I create a cash flow forecast if my business is brand new?

Start with what you know. Base inflows on signed contracts, your sales pipeline, and conservative estimates, always using the lower number when unsure. For outflows, list every planned expense, including startup costs. Your first few months will be estimates, and that's expected. Update it monthly as real data comes in, and it will get more accurate over time.

How often should you update your cash flow forecast?

Monthly at a minimum. On the last day of each month, compare your projection with what actually occurred, revise the coming three to six months according to the new information, and carry forward the forecast. When you are experiencing a tight time, change to weekly updates. A forecast you build once and never touch again doesn't protect you from anything.

Follow Vinay Kevadiya