Most founders finish their financial projections and feel one of two things: either quietly confident or quietly unsure whether any of it is actually realistic. If you've felt the second one, that's usually a signal worth paying attention to.

I've seen this moment catch founders completely off guard, and it's not because they can't do math. Most financial projection mistakes in a business plan come down to the assumptions underneath the numbers: where they came from, whether they hold up, and whether they connect to how the business actually works.

That's the gap most founders run into when learning how to create financial projections: overestimated revenue, missed costs, or numbers that look fine in a spreadsheet but fail when scrutinized.

If that sounds familiar, this blog is for you. I'll walk through the 10 most common financial projection mistakes, why they happen, and give you a specific fix for each.

The 10 financial projection mistakes at a glance

Here’s the short version; then we’ll go through each one in detail:

- Overestimating revenue: Assumes demand without showing how customers are actually acquired

- Confusing profit with cash flow: Shows profit while the business runs out of cash

- Underestimating expenses: Ignores small, recurring, and compounding costs

- Using top-down assumptions: Relies on market size instead of actual sales drivers

- Building only one scenario: Assumes one outcome and ignores uncertainty

- Not updating projections: Keeps outdated numbers despite real-world changes

- Ignoring seasonality: Assumes consistent revenue across all months

- Leaving out the founder's salary: Inflates profit by excluding real operating costs

- Hockey stick growth: Shows sudden spikes without a clear reason

- Not documenting assumptions: Uses numbers without explaining their source

Mistake #1: Overestimating revenue

Most first-time business plans show a version of the same curve. Slow start, then a sharp jump. Investors have seen it enough times to question it immediately.

The issue isn't ambition. It's how the number is built.

Two things usually drive this. First, optimism. When you're close to the idea, it's easy to assume demand will show up quickly. Second, market size gets mistaken for actual traction. Saying "we'll capture 1% of a $10M market" sounds grounded, but it skips how those customers are reached, converted, and retained.

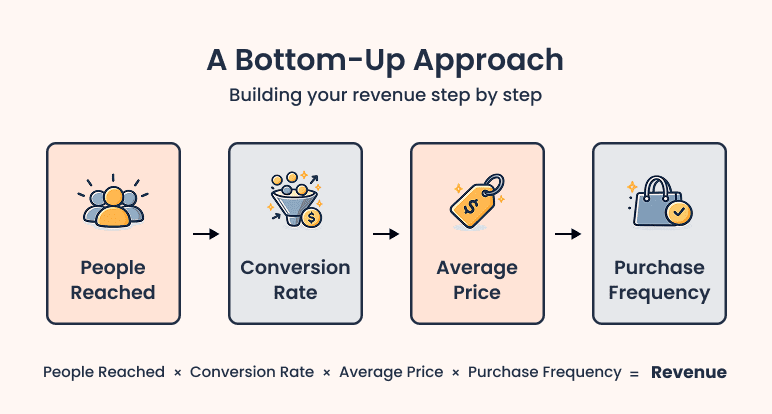

A more reliable approach starts at the ground level. Instead of starting with market share, you start with inputs you can actually explain:

How many people can you reach → how many convert → what they pay → how often they buy

For example: 100 customers × $80/month × 12 months = $96,000. Same number, but now there's a clear path behind it.

What I think most people miss is that revenue isn't just a demand problem; it's a capacity problem. Your projection should reflect how many customers you can realistically handle given your time, team, and channels. If that constraint isn't visible, the number is likely overstated.

Mistake #2: Confusing profit with cash flow

Profit and cash are treated as the same thing. They're not. It's one of the most common financial forecasting mistakes, and one of the most costly.

Profit is recorded when you earn revenue. Cash shows up when you actually get paid. That gap is where problems start.

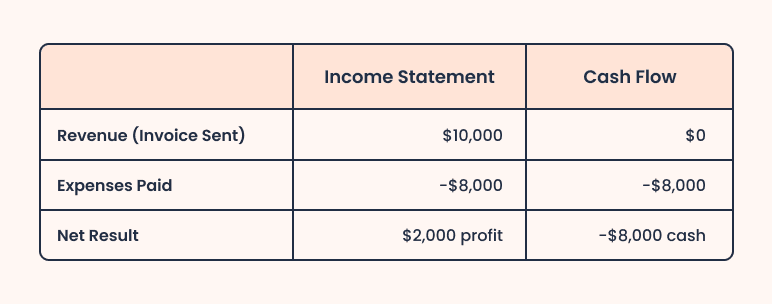

Say you invoice a client $10,000 in March. Expenses that month are $8,000, and paper profits are $2,000. But if that client pays net-60, you've spent $8,000 and received nothing. That's a cash gap.

I'd advise building a cash flow forecast alongside your income statement and treating them as a pair, not two separate documents. If you're putting together a business plan for a loan, lenders look at cash flow first because it's the only thing that tells them whether your business can actually make repayments. Profit on paper doesn't pay back a loan. Cash does.

Here’s an example:

Mistake #3: Underestimating expenses (Especially the small ones)

Most expense projections don't break because of one big miss. They break because of a lot of small ones that never made it onto the list.

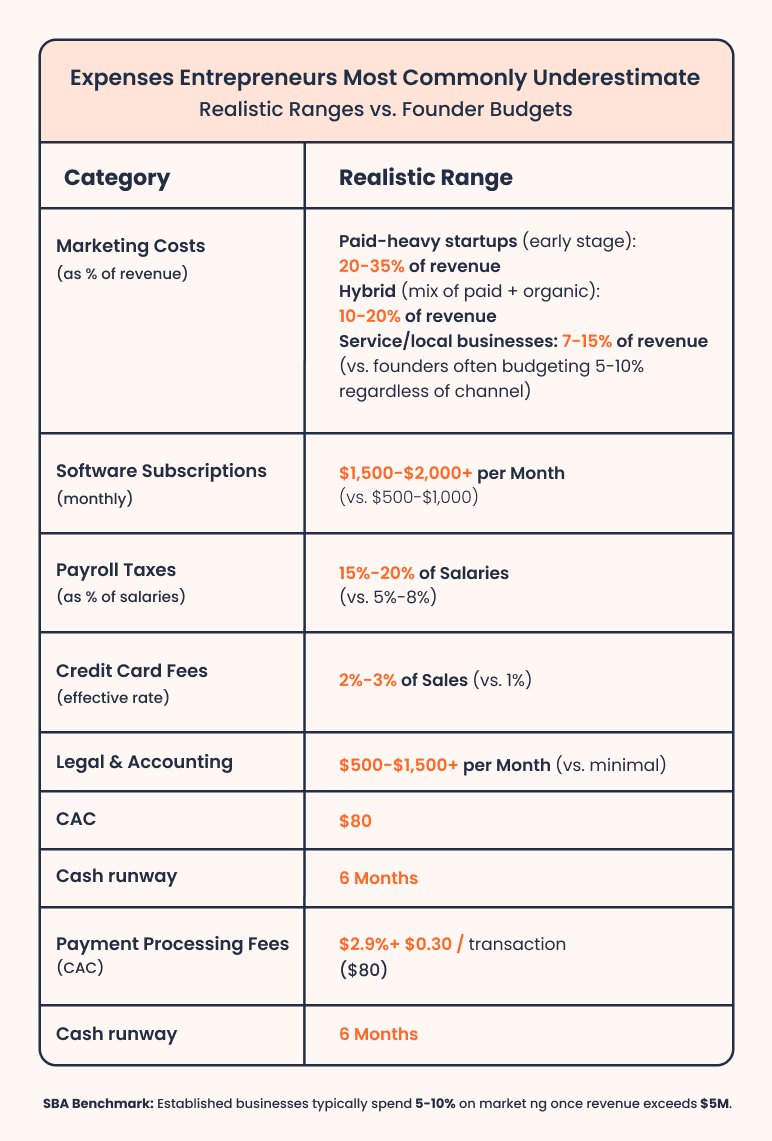

The obvious costs usually get covered: rent, salaries, and a rough marketing budget. But once the business starts running, more layers show up. Marketing alone rarely stays at 5% of revenue.

The obvious costs usually get covered: rent, salaries, and a rough marketing budget. But once the business starts running, more layers show up. Marketing alone rarely stays at 5% of revenue.

Operating costs follow the same pattern. Individually, they look manageable. Together they add up fast:

- Software stack (Slack, Notion, CRM, analytics, email tools) can cross $1,500–$2,000/month, and most tools are priced per user, so costs scale faster than founders expect

- Payroll taxes add a significant layer on top of salaries

- Payment processing fees (Stripe and PayPal both charge around 2.9% + $0.30 per transaction) eat into margins faster than most founders budget for

- Legal and accounting costs show up earlier than expected

- Annual renewals hit in lumps, not evenly

Fixed costs are usually planned well. It's the variable and compounding ones that founders consistently get wrong. I'd recommend starting with a base expense list, then pressure-testing it. Adding a 15–20% buffer to variable costs isn't exact, but it keeps projections closer to reality.

Mistake #4: Using top-down market assumptions

Saying "we'll capture 2% of a $5 billion market" is not a revenue projection. It's a placeholder for a number you haven't built yet.

The problem isn't the market size, really. It's that this approach skips how customers actually show up. There's no clarity on who you're reaching, how they convert, or why they'd choose you. Investors pick up on this quickly because the mechanism is missing.

Bottom-up projections fix this. Start with reach, not share:

- 2,000 people visit your site each month

- 3% convert → 60 customers

- Average order value: $50

- Purchase frequency: once per month

That gives you: 60 × $50 × 12 = $36,000 in annual revenue.

Every input is explainable. If your assumptions shift, the number shifts with them. That's what makes it something you can actually defend.

Mistake #5: Building only one scenario

Most single-scenario projections assume customers arrive on schedule, costs stay flat, and nothing unexpected happens. That's not how it goes.

A SaaS founder might project 50 new customers in Month 3. If they get 20 instead, the whole model is wrong, and there's no version of the plan that accounts for it. No adjusted runway, no revised burn rate, nothing to show an investor or lender when reality diverges.

This matters even more in a 3-year financial projection. Over that timeframe, something will deviate. If you assume it won't, the whole model becomes fragile.

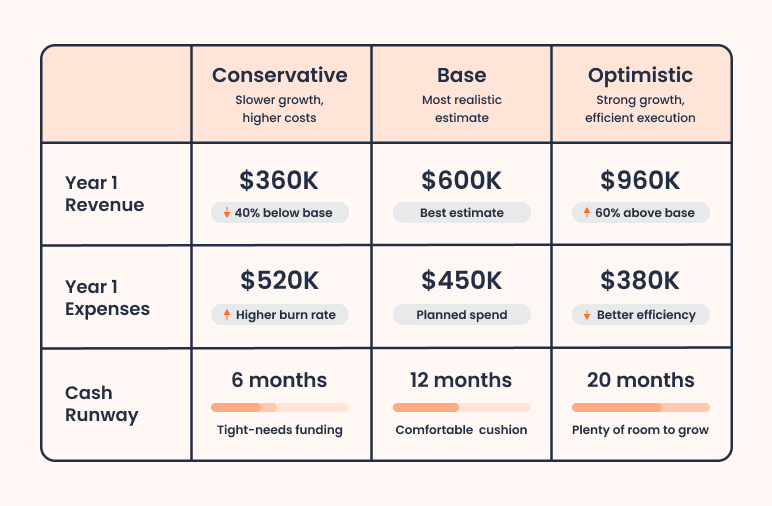

I recommend modeling three scenarios instead:

- Conservative: growth is slower, costs are higher, timelines stretch

- Base: your most realistic estimate

- Optimistic: stronger conversion, faster sales, better retention

Mistake #6: Not updating your projections after launch

Most founders build their projections before launch and never look at them again. I get why. Updating the numbers means acknowledging that timelines slipped, conversion didn't hold, or costs came in higher than expected. That's uncomfortable. So the model stays frozen while the business keeps moving.

Once you're operating, every month gives you real data. Ignoring it means your projection is just a document, not a tool.

Update monthly for the first year, then quarterly after that. And if any of these happen, don't wait for the next scheduled review:

- Revenue is off by more than 20% for two consecutive months

- A major cost shift, like a new hire, a rent increase, or a supplier change

- A revenue stream is added or paused

The goal is to keep the numbers honest.

Mistake #7: Missing seasonal swings

Almost no business earns the same amount every month. But most small business financial projections assume it will.

It's not always intentional. When you don't have past data, it feels easier to spread revenue evenly across the year and move on. The problem is that most businesses have patterns, and ignoring them makes cash flow unpredictable even when the annual total looks fine.

Seasonality shows up in places people don't expect. Retail and tourism are obvious, but even B2B and professional services have distinct patterns. A B2B consulting firm, for example, might see 40% of its annual revenue in Q1 and Q4 when budgets open and close, and just 10% in summer months.

December is another common dip. Usually, deals slow down, budgets get paused, and revenue drops, even though projections often show steady growth through the month.

If you're early and don't have historical data yet, I'd look at:

- Industry reports or trade associations

- Competitor filings or public benchmarks

- Google Trends for your product category

Even rough patterns are better than assuming consistency. Once you know where demand rises and falls, your projections start to reflect how the business will actually move through the year.

Mistake #8: Leaving out founder’s salary

If you're not paying yourself, your projections are inaccurate. They're showing a profit that only exists because you're working for free.

Most founders do this early on. The salary line gets removed to make the numbers look cleaner, or because the plan is to figure it out later. I understand the logic, but it creates a distorted picture. The business looks profitable on paper, but only because one of its core operating costs is missing.

Investors notice this quickly. If the model only works without paying the founder, it raises an obvious question: what happens when the business needs to operate sustainably?

A practical fix is to include a reduced but realistic salary. Start with your previous compensation and bring it down 30–40% to show commitment. That keeps the cost in the model without overstating it.

Mistake #9: The hockey stick projection

The hockey stick projection is so common it has a name. Investors have one too for what happens when they see it: a pass.

You've probably seen it. Revenue stays flat for a few months, then suddenly shoots up. The problem isn't the growth. It's that nothing in the model explains it.

From what I've seen, founders don't do this carelessly. They genuinely believe growth will kick in once things get going. But the model assumes momentum without showing what creates it, and that's what makes it hard to defend in a conversation.

If you genuinely expect a jump in revenue, show what drives it:

- A paid campaign with a defined budget

- A partnership that expands your reach

- A product launch or pricing change

The moment growth is tied to a specific action, it becomes something you can defend.

Mistake #10: Not writing down your assumptions

At some point in almost every investor conversation, someone asks a simple question: Where did this number come from?

Most founders know the answer when they're building the model. Six months later, sitting across from an investor, that answer is gone. The number is still there. The reasoning isn't.

That's the problem with undocumented business plan assumptions. They feel obvious when you make them. They become impossible to defend later.

Before any investor meeting, I'd have a clear answer for each of these:

- What's your customer acquisition cost, and where does it come from?

- How did you arrive at your average order value?

- What's your churn assumption based on?

- Where did your gross margin benchmarks come from?

If the answer to any of these is "I estimated," that's a red flag. "Based on IBISWorld industry benchmarks and three competitor pricing pages" is a real answer.

What investors actually red-flag when they review your projections?

Investors have reviewed hundreds of business plans. Most can tell within 90 seconds whether a projection was built or just assembled.

From reviewing hundreds of plans, they're not reading line by line. They're scanning for signals. Here's what tends to raise concerns immediately:

- Identical expense percentages every year: Signals copy-paste modeling, not real cost behavior

- Profits showing up too early: In competitive markets, early profitability without trade-offs feels unrealistic

- No cash flow statement: Suggests the founder hasn't thought through how money actually moves

- Round numbers everywhere: Flat $10,000 monthly expenses or neat growth rates usually mean the numbers weren't pressure-tested

- No mention of customer acquisition cost: If CAC isn't in the model, growth isn't explained

- High burn with no funding plan: Running out of cash with no clear next step signals poor planning

Investors aren't expecting perfect projections. They're checking whether you understand how your business behaves when things don't go as planned. A projection that shows where it might break often builds more confidence than one that only shows upside.

How does Bizplanr's AI handle financial projections for you?

Most of the mistakes in this list happen because spreadsheets have no guardrails. You can build something that looks complete and still be missing a cash flow statement, unlinked assumptions, or a scenario you never tested.

A 2025 US Bank survey found that 36% of small business owners are now using AI tools across their business, including for data analysis and financial planning, largely because the structural work is easy to get wrong manually.

Bizplanr's financial forecasting feature handles that structure. You put in your revenue streams, costs, and assumptions. It builds the income statement, cash flow, and balance sheet automatically and keeps all three linked. There's also a built-in AI advisor that reviews your numbers and flags gaps before an investor does.

Conclusion

Across all 10 mistakes, two patterns show up consistently. Founders overestimate outcomes without showing what drives them. And they treat projections as a one-time exercise, building them once and leaving them unchanged as the business evolves.

If you're preparing for a lender or investor meeting, start with Mistakes #1, #2, and #10. Those are the ones that get caught first.

Strong projections don't depend on accuracy. They depend on clarity: where the numbers come from, how they change, and what happens when things don't go as planned.

Before your next investor conversation, lender meeting, or planning session, I'd review your projections against this list. Fix the gaps, document your assumptions, and pressure-test your numbers.

For a deeper breakdown, read this guide on how to create financial projections.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

Do investors actually believe startup financial projections?

Not really, and that's not the point. Investors use projections as a thinking test. They want to see whether you understand your own business, not whether your Year 3 numbers will be right. Realistic assumptions with a clear source signal a founder who has done the work. A hockey stick with no explanation signals the opposite. For a financial projections example built the right way, see our step-by-step guide.

How do you create financial projections when you have no sales history?

Start with your customer acquisition plan, not your market size. If you expect 2,000 site visitors a month and a 3% conversion rate, that's 60 customers. Multiply by your average order value and purchase frequency. That's a projection. "We'll capture 1% of a $5M market" is not. Use conservative assumptions, show your working, and build from inputs you can actually explain.

How often should you update financial projections?

It depends on where you are. Pre-revenue, quarterly is usually enough since there's no real data to react to yet. Once you launch, move to monthly. After you've raised funding or hit consistent revenue, quarterly works again, but only if you have a trigger system in place for major changes. The earlier you are, the more frequently you should be looking at your numbers.

What's the difference between financial projections and a financial forecast?

Projections show what could happen under a specific set of assumptions. They're used for planning and fundraising. Forecasts reflect what's most likely based on current trends and are used for day-to-day decisions. Most early-stage founders need projections. Once you have 6 to 12 months of real data, switching to a rolling forecast gives you a more useful planning tool.

What are the three financial statements every business plan needs?

An income statement covering revenue, expenses, and profit or loss. A cash flow statement shows when money actually moves in and out. And a balance sheet covering assets, liabilities, and owner equity. The mistake most founders make is building them separately. All three need to be linked. A change in one should flow through to the others automatically.

Follow Kaylee Philbrick-Theuerkauf