One of the quickest ways of getting into trouble is operating a business without having a financial forecast. Indeed, 82% of businesses are failing because of cash flow issues that arise from poor forecasting.

Financial forecasting involves trying to predict the financial performance of your business in the future, depending on:

- Current data

- Assumptions

- Expected market conditions

It assists you in estimating the amount of income you will receive, the amount you will spend, and also whether to keep a sufficient amount of cash to run smoothly or not.

When developing a business plan, raising capital, or just defining your business plan assumptions, you need to know financial forecasting.

What is financial forecasting?

Financial forecasting refers to the predictive process that is made on the future performance of the business based on previous data, present performance, and practical assumptions.

Let me explain with an example: You're opening a bakery in Austin, Texas. You are planning to sell 80 loaves of bread per day at a price of $8, buy ingredients that cost you $3,200 every month, and rent costs you $2,500. That is a financial forecast of 12 months projected in math. It won't be perfect. However, it provides you, your banker, and any prospective investor with a systematic method to know whether the business is viable.

A complete financial forecast typically connects three core financial statements:

- An income statement projects your revenue, costs, and profit over time.

- A cash flow statement tracks when money actually comes in and goes out.

- A balance sheet shows what your business owns and owes at a future point.

However, a forecast is not a guarantee. It’s an informed estimate built on assumptions. Investors and lenders don’t expect perfect accuracy. They look for logical reasoning, realistic inputs, and consistency.

Forecasts can be short-term, such as monthly projections for the next year, or long-term, covering three to five years. In most cases, these forecasts become a core part of your business plan, especially when you’re seeking funding or planning growth. Now, about the forecasting period, forecasts can be short-term, such as monthly projections for the next year, or long-term, covering three to five years. In most cases and business plans, you need both short-term and long-term projections.

Why financial forecasting matters for your business

Financial forecasting can become the financial backbone of your business. Everything else, your marketing spend, your hiring timeline, and your funding ask, can trace back to it.

From a lending perspective, banks won’t lend you money without a financial forecast. Neither will most investors. Before anyone puts money into your business, they want to see clear, numbers-backed expectations of how it will perform.

Here are more reasons why financial forecasts matter:

| Why It Matters | What It Means for Your Business | Example |

|---|---|---|

| Securing funding | Lenders and investors use your forecast to evaluate risk, repayment ability, and growth expectations | A bank reviews your 3-year coffee shop forecast showing $20,000 monthly revenue before approving a loan |

| Managing cash flow | Helps you track when money comes in vs. goes out so you don’t run out of cash | Your coffee shop earns $20,000 in sales, but supplier payments of $6,000 are due earlier, creating a cash gap |

| Hiring and spending decisions | Guides when you can afford to hire, invest, or expand without overextending | You delay hiring a third barista until your monthly profit consistently crosses $5,000 |

| Setting revenue targets | Turns vague goals into clear, numbers-based targets tied to pricing and sales volume | You plan for 85 customers/day × $9.50 × 26 days = ~$21,000 monthly revenue |

| Preparing for uncertainty | Allows you to plan for best, expected, and worst-case scenarios | You model a worst-case scenario with 60 customers/day and adjust expenses to stay profitable |

Update your forecast every month, not just when you're raising money. Compare what you projected against what actually happened. That gap, positive or negative, is where the real business lessons are.

5 Types of financial forecasts you should know

Financial planning and forecasting are not about making tables and columns and filling in numbers. Your every need has a different type of financial forecasting. The type you need depends on what question you're trying to answer. Some forecasts focus on growth, others on costs, and some on whether you’ll have enough cash to stay operational.

Here is what different financial forecasting models do and when you actually need them:

| Forecast Type | What It Predicts | When to Use It |

|---|---|---|

| Revenue forecast | Estimates how much money your business will generate over a specific period based on pricing, sales volume, and demand | Use this when setting sales targets, validating your business idea, or building the top line of your business plan |

| Expense forecast | Projects your future costs, including fixed expenses (rent, salaries) and variable costs (materials, marketing) | Use this to understand how much it will cost to operate and to control spending as your business grows |

| Cash flow forecast | Tracks when cash actually comes in and goes out of your business, not just when sales happen | Use this to avoid running out of cash, especially if you have delayed payments or upfront expenses |

| P&L (profit and loss) forecast | Combines revenue and expenses to show your expected profit or loss over time | Use this to evaluate profitability and determine whether your business model is financially viable |

| Balance sheet forecast | Projects what your business will own (assets) and owe (liabilities) at a future point | Use this when preparing for loans, investors, or understanding long-term financial health |

Which forecast type do you need first?

You will need all five in case you are writing a business plan. The combination of them creates a complete financial picture that the lenders and investors want to see.

To begin with, a cash flow forecast in case you have an existing business. It has a direct impact on your capacity to cover bills, run a business, and survive, even though your revenue might appear healthy on paper.

Financial forecasting methods: Quantitative vs. qualitative

Before we understand the methods, let’s first look at what quantitative and qualitative forecasting actually mean.

Quantitative forecasting involves the use of past information and figures to determine future performance. Businesses with a history of sales that desire additional data-driven projections are likely to use it.

Qualitative prediction is based on the judgment, research, and input of experts rather than previous information. Mostly, it is applied to startups or a business venturing into new markets where there is limited or no historical data.

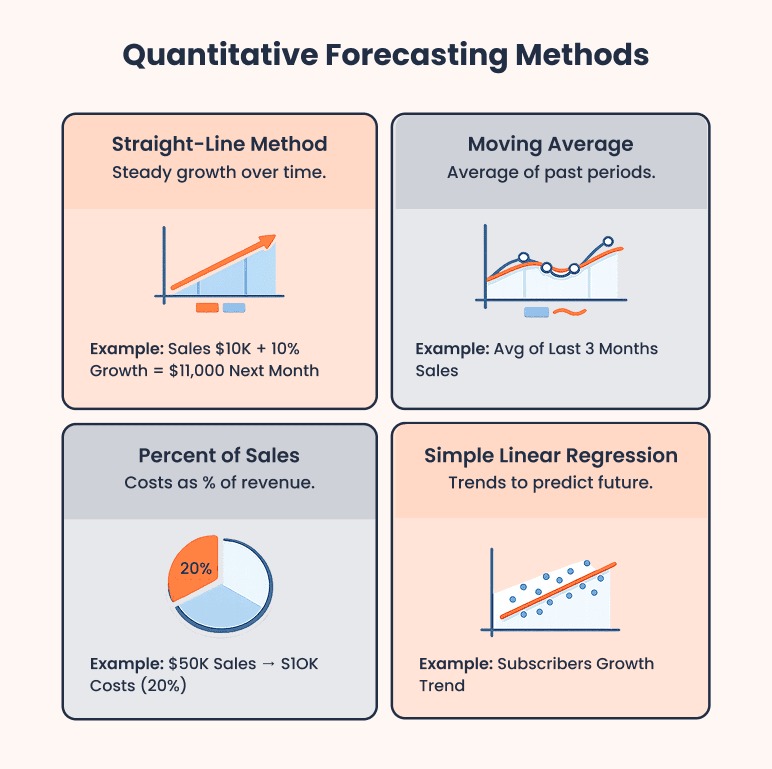

Quantitative forecasting methods

Quantitative methods are math-based. They take historical numbers and use formulas to project what comes next. These work best when you have at least 6-12 months of actual business data to draw from. Here are the quantitative forecasting methods that you can use:

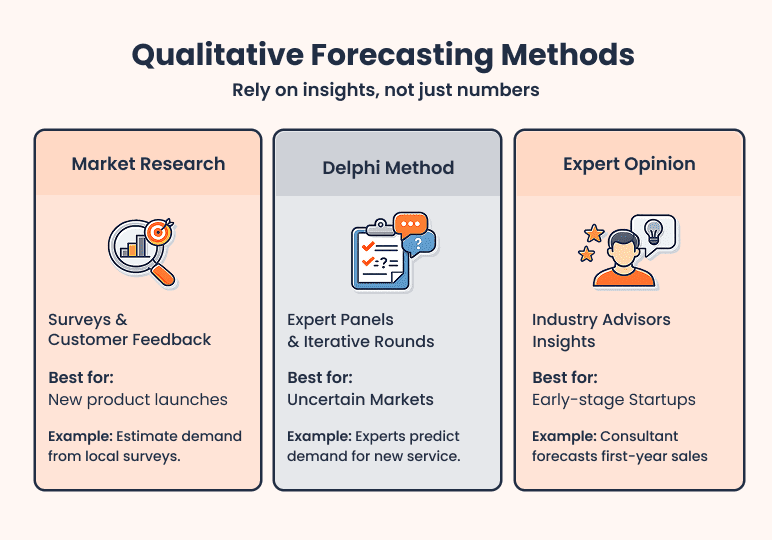

Qualitative forecasting methods

Qualitative methods rely on judgment, research, and external inputs instead of past data. These are useful when you don’t have enough historical numbers, especially in the early stages of a business or when entering a new market. Here are the qualitative forecasting methods that you can use:

Where These Methods Work Best (and Who Should Use Them)

Choosing the right forecasting method depends on how much data you have and how stable your business is. Using the wrong method often leads to unrealistic projections or overcomplicated models.

- Early-stage founders with no sales history should rely on qualitative methods like market research and expert input

- Small business owners with 6–12 months of data can use simple quantitative methods like straight-line or percent of sales

- Businesses with consistent historical data can apply moving averages or regression for better accuracy

- Businesses entering new or uncertain markets should lean on qualitative methods to estimate demand

- Growing businesses should combine both methods to balance real data with future assumptions.

Which method should you use?

Use this as your quick decision guide:

| Your Situation | Recommended Method |

|---|---|

| New business, no revenue history | Market research + expert opinion |

| 6–12 months of data available | Straight-line or moving average |

| Expenses tightly tied to sales volume | Percent of sales |

| Two variables with a clear relationship | Simple linear regression |

| Complex market with high uncertainty | Delphi method |

| Writing a business plan from scratch | Start qualitative, then build in quantitative |

For most small businesses, a simple straight-line forecast with 3 scenarios is more useful than a complex regression model you can't explain to investors.

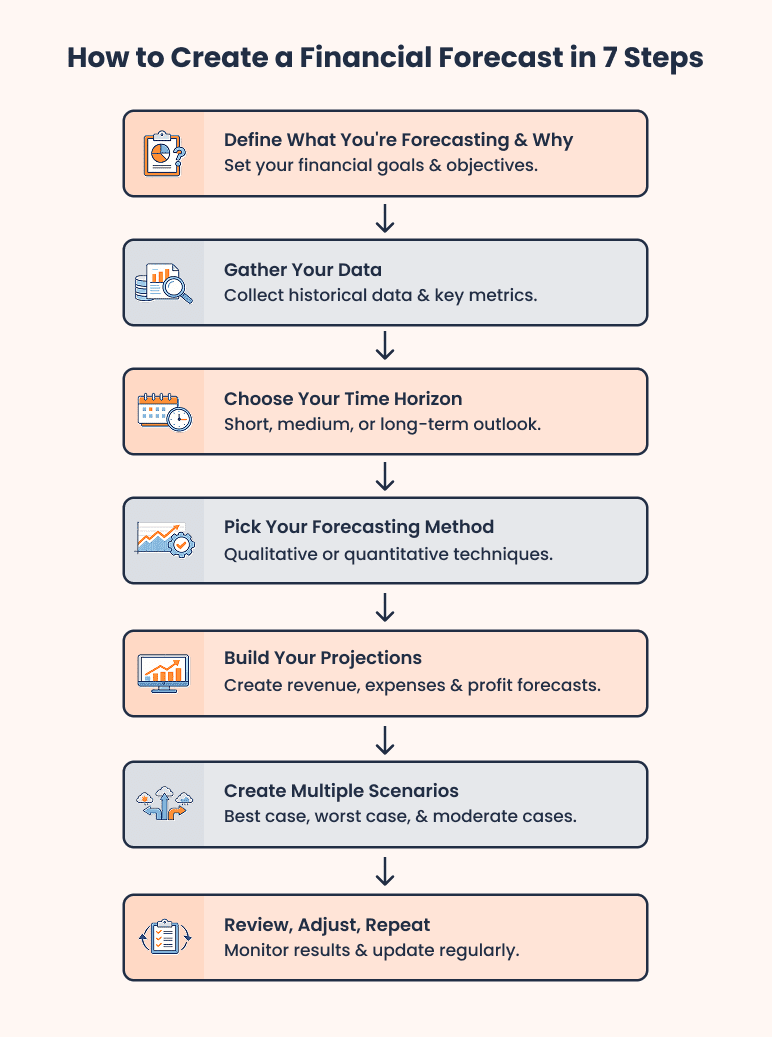

How to create a financial forecast in 7 steps

Whether you’re starting from scratch or refining an existing plan, these steps help you build clear and practical projections.

Let’s walk through this using a simple example: A new coffee shop planning its first year of operations.

Step 1: Define what you're forecasting and why

Before you touch a single number, get clear on the purpose. Are you writing a business plan for an SBA loan? Pitching an investor? Planning your first year of operations? The purpose determines how detailed you need to be and which statements matter most.

For example, the coffee shop owner is applying for a $75,000 SBA loan. That means the lender needs a full set of projections, including a P&L, cash flow statement, and balance sheet. That's our deliverable for this exercise.

Deliverable: Define purpose + list of outputs needed (revenue, expenses, cash flow).

Step 2: Gather your data

Pull together everything you have. For a new business, that includes:

- Market research

- Local foot traffic estimates

- Competitor pricing

- Industry benchmarks

- Expected startup costs

For an existing business, pull your last 12 months of actual financials.

Let’s understand with our coffee shop example: The owner has to research average revenue per square foot for coffee shops (roughly $400-$600/sq ft annually per industry data), check competitor menu pricing on Yelp, and collect quotes from suppliers for beans, cups, and dairy. The owner also pulls the lease agreement ($3,800/month) and equipment financing terms.

Your deliverable: A research folder with pricing data, cost quotes, market size estimates, and any comparable business benchmarks you can find.

Step 3: Choose your time horizon

For a business plan, I recommend 12 months of monthly projections plus a 3-year annual summary. The monthly detail shows lenders you understand cash timing. The 3-year view shows investors a growth trajectory.

For our coffee shop: Month 1 through Month 12 broken down monthly, then Year 2 and Year 3 shown as annual totals. That covers the SBA lender's requirement completely.

Your deliverable: A blank spreadsheet or forecasting template with the correct time columns already set up.

Step 4: Pick your forecasting method

With no revenue history, our coffee shop owner uses a bottom-up market research approach. She estimates daily customer count based on foot traffic, average spend per visit, and days open per month. That's her revenue engine.

For expenses, the owner uses a percentage of sales for variable costs (coffee supplies, packaging) and fixed monthly amounts for everything else (rent, payroll, utilities, insurance).

Your deliverable: A clear decision on which method drives your revenue projection and which drives your expense projection.

Step 5: Build your projections

Now turn assumptions into numbers. Calculate revenue, costs, and profit. Here's what Month 1 looks like for our coffee shop:

| Line Item | Value |

|---|---|

| Estimated daily customers | 85 |

| Average spend per visit | 10 |

| Operating days | 26 |

| Projected Revenue | $22,100 |

| Cost of goods sold (32%) | $7,072 |

| Rent | $3,800 |

| Payroll (2 part-time staff) | $5,200 |

| Utilities | $420 |

| Insurance | $180 |

| Miscellaneous | $300 |

| Total Expenses | $16,618 |

| Net Profit | $4,377 |

Your deliverable: A completed Month 1 projection for revenue, expenses, and net profit. Then replicate across all 12 months, adjusting for seasonality and planned changes.

Step 6: Create multiple scenarios

A single forecast is just an estimate. Building three scenarios—base case, expected case, and optimistic case—turns your forecast into a practical plan.

For our coffee shop, the base case assumes 85 customers/day. The expected case drops to 60 customers/day for the first three months, reflecting a slower ramp-up. The optimistic case assumes a strong opening with 110 customers/day by month 3, due to a local PR push.

Lenders and investors don't expect you to be right. They want to see that you've thought through what happens if you're wrong.

Your deliverable: Three versions of your Month 1-12 P&L: base, conservative, and optimistic.

Step 7: Review, adjust, repeat

Once the business is running, compare your actual numbers against your projections every single month. Where you're off, ask why. Then update the forecast forward.

For our coffee shop: By Month 2, the actual customer count is averaging 72/day instead of the projected 85. The owner adjusts Months 3-12 downward, recalculates cash flow, and identifies that they’ll need a $4,000 cash cushion by Month 5. The owners have time to plan for it because they caught it early.

Your deliverable: A monthly calendar reminder to run a plan vs. actual comparison and update the forward projection.

If spreadsheets aren't your thing, tools like Bizplanr can automate these calculations.

Financial forecasting vs. budgeting: What's the difference?

If you think forecasting and budgeting are the same, you’re not alone, but they serve different purposes. Here’s the simple difference.

A financial forecast predicts what is likely to happen in your business based on current data, trends, and assumptions. A budget, on the other hand, is your plan for how you intend to spend and allocate money over a specific period.

| Basis | Budget | Forecast |

|---|---|---|

| Purpose | Sets spending limits and financial targets | Predicts actual financial performance |

| Focus | What you plan to do | What is likely to happen |

| Timeframe | Usually fixed (annual or quarterly) | Flexible and ongoing |

| Flexibility | Static rarely changes | Adjusts as business conditions change |

| Update frequency | Set once, reviewed periodically | Updated regularly (monthly or quarterly) |

In simple terms, a budget is your financial plan, while a forecast reflects your current reality. The practical approach is to build your forecast first, then create a budget around it.

Financial forecasting for your business plan

Financial forecasting isn’t an option if you’re preparing a business plan for a bank loan, investor pitch, or SBA application. In fact, it’s one of the first sections lenders and investors review to decide whether your business is worth backing.

At a minimum, they expect a 3-5 year financial forecast that covering three core statements:

- Income statement (revenue, cost of goods sold, operating expenses, net profit)

- Cash flow statement (cash inflows, cash outflows, opening and closing balance)

- Balance sheet (assets, liabilities, equity)

What changes is the level of detail depending on who you’re pitching to.

- Banks and SBA lenders focus on risk and repayment. They expect conservative projections, clear monthly cash flow (especially Year 1), and realistic assumptions.

- Angel investors care more about growth and upside. They look for scalable revenue, strong margins, and how quickly the business can expand.

Most reviewers don’t start by reading everything. They scan for three things first:

- Is the revenue realistic and clearly explained?

- Does the cash flow stay positive or manageable?

- Do the assumptions make sense for the industry?

Your assumptions matter as much as your numbers. Pricing, customer volume, growth rate, and costs should all be clearly explained and tied to logic.

The key is clarity. Show how your numbers are built, not just what they are.

If you’re unsure how to structure this section, refer to a detailed guide on how to build the financial projections section of your business plan. Tools like Bizplanr’s financial forecasting feature can also help you generate these statements quickly and organize them in a format that lenders expect.

How startups can forecast without historical data

When you don’t have past numbers, your forecast depends on research and logical assumptions. The goal is not perfection but showing that your numbers are realistic and well thought out.

You start by using external data to build a foundation, then layer your own assumptions on top. Instead of guessing, you rely on simple calculations and real-world references to create a practical forecast.

- Use industry benchmarks from sources like SCORE, Bureau of Labor Statistics, or Statista to understand average costs, margins, and performance

- Build a bottom-up forecast using basic drivers like customers, pricing, and purchase frequency to estimate revenue

- Apply market sizing (Total Addressable Market, Serviceable Available Market, Serviceable Obtainable Market) to understand your growth opportunity and support long-term projections

- Study similar businesses to validate your assumptions around pricing, growth, and cost structure

A strong forecast without historical data comes down to clear logic, realistic assumptions, and a simple, explainable model.

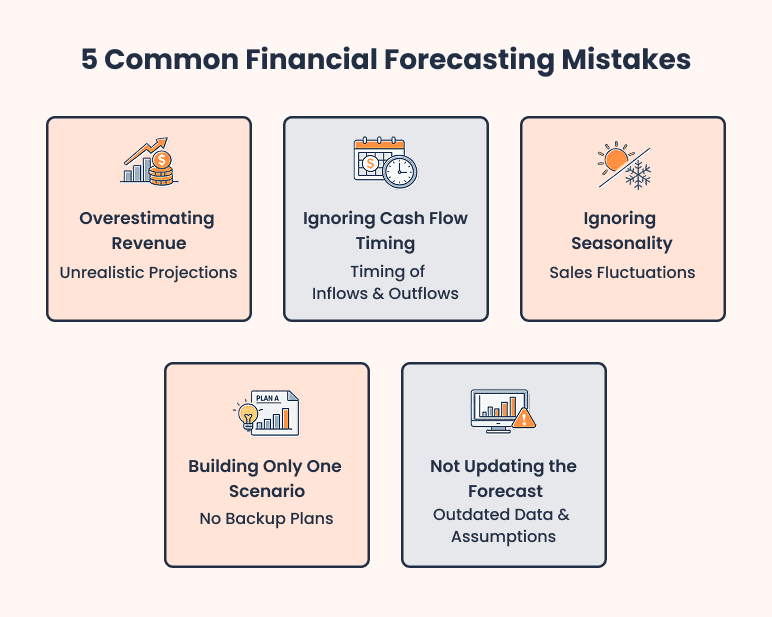

5 Common financial forecasting mistakes (and how to avoid them)

Most forecasts don’t fail because of bad math. They fail because of unrealistic business plan assumptions and poor thinking. Here are the most common mistakes that owners make when preparing financial forecasting:

- Overestimating revenue (the hockey-stick trap)

- Ignoring cash flow timing

- Ignoring seasonality

- Building only one scenario

- Not updating the forecast

Let’s discuss each mistake in detail. Many founders assume rapid growth without clear reasoning means overestimating revenue. Doing this will surely look good on paper, but won't hold up.

Now, second, assuming revenue as cash is another mistake that many founders make. Revenue does not mean cash in hand. You might make a sale today, but get paid 30 or 60 days later. Thus, always create a cash flow forecast alongside your revenue forecast. Map when money actually comes in and goes out.

The third mistake is ignoring seasonality. Sales are rarely consistent throughout the year. Many businesses have peak and slow periods. Adjust your forecast for seasonal trends. Use industry data or similar businesses to estimate high and low months.

Then relying on a single forecast assumes everything will go as planned, which rarely happens. Create at least three scenarios: best case, expected case, and worst case.

Lastly, a forecast quickly becomes outdated if you don’t update the forecast based on actual performance. So, review your numbers monthly and update them regularly.

Remember, financial projection mistakes are not about wrong formulas but about flawed assumptions and a lack of regular updates.

How Bizplanr makes financial forecasting easy

Building financial forecasts from scratch can feel overwhelming, especially if you’re not comfortable with spreadsheets or financial modeling.

Bizplanr simplifies this process by using AI financial forecasting based on your business type and inputs. Remember the coffee shop forecast? With Bizplanr, you enter your inputs, and the AI builds your statements in minutes.

Instead of starting with a blank sheet, you get a structured forecast tailored to your business model, saving hours of manual work.

Our financial forecasting software automatically creates all the key financial statements you need, including your income statement, cash flow statement, and balance sheet. These are organized in a format that lenders and investors expect, so you don’t have to worry about structure or presentation.

Using our financial forecasting tools can also generate multiple scenarios, such as best case, expected case, and worst case. This helps you understand how changes in sales, costs, or assumptions affect your business.

Once your forecast is ready, Bizplanr lets you export investor-ready documents that you can directly include in your business plan or share with stakeholders.

If you want to explore how it works, check out the financial forecasting feature or try the tool to build your projections.

Use Bizplanr AI to create a first draft of your forecast, then refine it with your own assumptions and research. It’s much faster than building everything from scratch.

Conclusion

Financial forecasting is not about getting every number right. It’s about being prepared and making informed decisions based on realistic assumptions.

By understanding your numbers, choosing the right method, and following a clear step-by-step process, you can build a forecast that actually supports your business growth.

Take the coffee shop example. You don’t need perfect data to start. You can begin with simple inputs like daily customers, average order value, and monthly costs, then refine as real data comes in.

Start simple, focus on logic over complexity, and update your forecast as your business evolves. If you want to save time and avoid starting from scratch, try Bizplanr’s AI financial forecasting tool to quickly generate and refine your projections.

Get Your Business Plan Ready In Minutes

Answer a few questions, and AI will generate a detailed business plan.

Frequently Asked Questions

How often should I update my financial forecast?

Review your forecast every month to track performance. Update it at least quarterly to keep it aligned with reality. If something significant changes, update it immediately.

How does inflation or rising costs affect my budget vs forecast?

A budget is fixed, so rising costs can quickly make it inaccurate. A forecast adjusts as costs change, helping you see the real impact on profit and cash flow.

What is the difference between financial forecasting and budgeting?

A budget is your plan for how you intend to spend and allocate money. A forecast shows what is likely to happen based on current data and trends. You usually build a forecast first, then create a budget around it.

How do startups create financial forecasts without historical data?

Financial projections for startups rely on external data and logical assumptions. They use industry benchmarks, build bottom-up projections based on pricing and expected customers, estimate market size using TAM, SAM, and SOM, and study similar businesses to guide their numbers.

Follow Vinay Kevadiya